|

More Victories For The Rule Of Law- Page Fifty-Four

Hundreds of thousands of readers of 'Cracking the Code- The Fascinating Truth About Taxation In America' have taken control of their own resources, in accordance with, and respect for, the law. The total amount reclaimed by these good Americans so far is upward of several billion dollars.

A few of these good American men and women-- such as those honored below-- are generous enough to send me the evidence of their victories in upholding the law, for the edification and inspiration of everyone. Gene Allen Gene has secured a complete refund from California of everything given to it during 2015 against the possibility that his earnings were from taxable activities. Having found that they were not, the state has returned every penny of Gene's property in response to his CtC-educated claim:

Here is the filing that produced this uplifting victory for the rule of law over the income tax myth-meisters who are trying desperately to keep more Americans from learning the truth about their myths, as Gene has done. Al Monteilh Al is an educated, grown-up American like Gene, who takes his civic duties seriously. Al has acted to ensure that the fine state of Colorado sticks to the rules, and doesn't persist in a bad habit of taking what doesn't belong to it by exploiting ignorance and fear. Colorado knows that games won't work on CtC-educated Americans. In response to a batch of educated claims Al filed earlier this year, Colorado coughed up a batch of complete refunds last month (all shot on a smart-phone, and hence a bit distorted-- and btw, Al is the one who added the smiley-faces...):

Here is the filing that produced this 2012 refund.

Here is the filing that produced this 2013 refund.

Here is the filing that produced this 2014 refund.

Here is the filing that produced this 2015 refund. W. & A. D. W. &. A. D. are sharing their first victory won on behalf of the rule of law as CtC-educated Americans with a complete understanding of the actual scope and requirements of the income tax levied in the USA. This first victory is a refund of amounts withheld in 2014 and given over to the federal government against the possibility that W. and A. might have actually engaged in taxable activities and owe income taxes accordingly (as opposed to their gains having been from untaxable economic activities, as most people's are). Unlike most refunds from educated filings, though, what W. & A. received so far is a "victory-in-progress". Here's what this means: The United States has returned every penny of what had been withheld from W. &. A. during 2014 under the normal "Subtitle A" tax provisions. In this case that was $5,187.47 (with interest included) which was withheld under the provisions of chapter 24 of Subtitle C of the code. That type of withholding gets set aside in an escrow account and then is credited against any tax which proves to be owing at the end of the year, with the balance being refunded. (See pp. 174-175 of CtC for the statutory provisions laying out this relationship.) The form 4852 W. &. A filed as part of their return/claim (see it here) shows the chapter 24 withholding as the nominal "federal tax withheld". Here is the IRS notice announcing W. & A.'s refund of this amount:

Here is the delivered refund:

The complete refund of this withheld amount is an agreement that W. & A. owed no tax for the year-- had they owed anything, this withheld amount would have been tapped to cover the liability. Indeed, the IRS explicitly acknowledges that W. & A. had no "income" and owed no tax, in harmony with this refund, on the second page of its notice:

So, everybody agrees that W. & A. had no "income". In particular (the significance of which will become clear in a moment), everyone agrees that W. & A. had received no "wages"-- that's the specially-labeled form of "income" under which chapter 24 withholding takes place, and the species of "income" upon which a Subtitle A tax will be presumed to have arisen in the case of workers like W. & A.. And again, everyone agrees W. & A. received no "income". But despite everyone agreeing that W. & A. had no "income" upon which a tax liability could arise, the IRS is still trying to get away with keeping a lot of W. & A.'s money. AS WILL HAVE BEEN NOTICED when looking at W. & A.'s sworn return/claim, and the 4852 included within it, W. & A. had a good deal more withheld than just the $5,187.47 they received back so far. In fact, W. & A.'s claim seeks $9,585.53-- the total of all amounts withheld from them. This total includes not just the nominal "federal income tax withheld" under provisions of Subtitle C's chapter 24 (the withholding for deposit against the "normal tax" under Subtitle A) but also the Social security and Medicare "income" taxes, which are withheld under the provisions of chapter 21 of Subtitle C (the withholding for the FICA "surtax" on "income"). The IRS is trying a gambit on W. & A., pretending that the surtax wasn't withheld, or somehow should be excluded from the total withheld. and hoping W. & A. won't realize what's going on. (Or the agency hopes the boldness and incoherence of the corrupt ploy will intimidate or confuse W. & A. into taking their partial refund and letting the rest go). I don't think so... This is another of the "Flailing Robot" desperation ploys of the sort presented on the Every Which Way But Loose pages.

"LOOK OUT, DOCTOR SMITH!! DANGER!! WARNING!!" But even as this little saga plays out as an obnoxious pain in the a** for W. & A., it is a wonderful illustration of the truth about the tax, the fact that the truth cannot be avoided or overcome, and that the only game the "ignorance tax" scamsters have is smoke and mirrors and lies and evasions. I sincerely hope that everyone will show their skeptical friends, family, and neighbors this dodgy Whack-a-Mole episode to illustrate the truth and wake them to their responsibilities as grown-up Americans responsible for seeing that the law is upheld (and for jealously safeguarding their own rights and property). S. Y. On May 19, 2016, Missouri was pursuing proposed tax liabilities against S. Y.. The liabilities were related to alleged taxable real estate sales transactions in 2006 totaling $135,500.00, which had been reported to the state DOR by the IRS:

Two months later, the tune had changed completely:

See the whole story here. Brian Wright

Here is the filing that produced this refund, complete, and with interest.

Georgia John GEORGIA JOHN SHARES A NICE VICTORY-- a complete recovery by an amended return of everything withheld and given over to Georgia in 2012, plus interest calculated for the three years the money sat where it didn't really belong:

Here is the filing that produced this victory.

The Walkers C. WALKER AND HIS LOVELY WIFE are good Americans. These two fine folks have taken measures to keep North Carolina within the bounds of the law and to keep their property and the power it conveys within their own sensible hands. North Carolina has proven to be a faithful public servant, returning every penny withheld from the Walkers during 2015 against a tax they never actually owed, their work not being of the taxable variety, plus interest:

Here is the filing that produced this victory.

Brian S.

This victory has a story... See it here.

Steven B.

Steven's filing can be seen here. Missouri began by balking at the claim, until Steven rebutted its pretense and the state gave up the resistance.

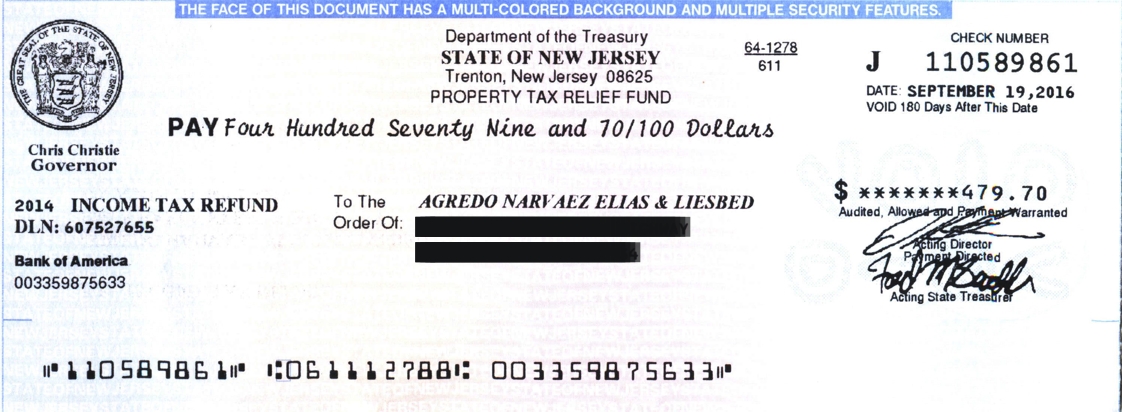

Elias & Liesbed Agredo-Narvaez

The filing by which this claim was made can be seen here.

Vincent & Shelly T.

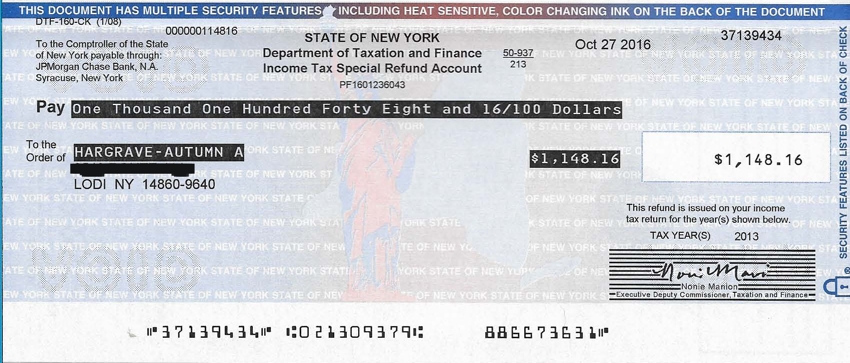

The refund was issued pursuant to this 1040 claim, but only after some tax-agency bad behavior. Two months after receiving Vincent and Shelly's claim in April of 2016, the revenue-hungry government pretended, by way of this notice, that it couldn't verify the withholding amounts Vincent and Shelly had declared. Victor and Shelly promptly replied, of course, with a good deal more courtesy than some would think appropriate. Along with pointing the agency to the undisputed sworn documents already provided, the couple included additional documentation of their refund claims. The government then challenged Vincent and Shelly's identities, by way of this notice. Upon getting the couple's phone call, the IRS gave up and issued their check. Autumn Hargrave Autumn proudly shares two victories secured in October 2016. These are complete refunds of everything withheld and paid over to the state as "income" tax during 2013 and 2014, respectively, both include interest, and both issued in response to amended returns. Here is the refund for 2013:

The filing (and the notice showing the interest computation) can be seen here. Here is Autumn's refund for 2014:

The filing (and the notice showing the interest computation) can be seen here.

Click here to return to the Bulletin Board

Even in the face of the requirements of the law, the junkyard dog still tries to play its losing hand occasionally. Ironically, it is these sporadic spasms of resistance that offer the most telling evidence of the truth about the tax...

Despite the fact that those whose victories are on display here did nothing but insist that the law be applied as it is written, they did so in the face of fearful threats and cunning disinformation from the beneficiaries of corruption. Their actions took great courage and commitment, and I salute them all.

“God grants liberty only to those who love it, and are always ready to guard and defend it.”

-Daniel Webster

NOTE: Whether any given individual is entitled to a refund depends on a number of different factors, and no one should presume that they are so entitled simply because they see that others are. Each person should educate himself or herself about the particulars of the law, and make his or her own determination in this regard.

To get on the Lost Horizons mailing list, send an email to SubscribeMe 'at' losthorizons.com with your name in the message field.

NOTE: The documents displayed on this and any linked pages, and any associated comments, are posted with the permission and cooperation of the upstanding Americans with whom they are concerned. When a return is posted in connection with any refund or other responsive document, it is complete-- that is, what is posted is EVERYTHING filed as a return in connection with that refund or document, unless otherwise indicated. |