|

The liberating truth about the "income" tax is turning those

who would evade it

Every Which Way But Loose Part III

A collection of undeniable evidence of the

correctness of

CtC

Do you remember those old sci-fi movies (and numerous 'Lost in

Space' and 'Star Trek' episodes) in which an evil robot or a

computer collapses into terminal dysfunction after being

presented with data that "does not compute"? The machine

would flail about dangerously for a bit (or smoke and shake, and

threaten to explode) before finally going limp, silent and

harmless.

"LOOK OUT, DOCTOR SMITH!! DANGER!! WARNING!!"

Some

CtC Warriors are being drafted to play the part of the

intrepid heroes of these space operas lately, with federal and

state "income" tax agencies in the role of the neurotic robot.

SINCE AUGUST OF 2003, when the revelations of

CtC were first published,

tens of thousands

of readers of 'Cracking

the Code- The Fascinating Truth About Taxation In America' have taken

control of their own resources, in accordance with, and respect for, the

law. The total amount reclaimed by these good Americans so far is

upward of several billion dollars.

During the same period,

the IRS has engaged in a

desperate struggle to regain its hold of fear and confusion over

those now equipped with an understanding of the long-hidden

secrets of the "income" tax, and to stop that understanding from

spreading. This effort has involved the resort to many (and

increasingly) bizarre evasions and theatrics.

IN THIS SERIES, we take a close look at many of these gimmicks,

ploys and dodges. The action in these episodes will range from silly

one-shot, quickly-abandoned agency stalls to drawn-out, elaborate

efforts to resist or evade or discourage

CtC-educated filers ending in dramatic slap-downs of the

law-defying tax agency.

One consistent feature of all of these episodes is

the special clarity with which they illustrate the accuracy and

completeness of what

CtC reveals about the "income" tax. Unlike the vast majority

of

CtC-educated refunds and other victories in applying the

law in which the

deep vetting to which every claim is subject is done out of

view, with no evidence of the process except the filing and the

check or transcript, what happens in the cases highlighted in

this series takes place only after unambiguous, close tax-agency

attention to the claim.

Thus, these cases present a wake-up splash of

reality to those who struggle to persist in denial about the

truth, completeness and correctness of

CtC (some of whom actually argue with a straight face that

the hundreds of thousands of complete refunds issued over all

those years now from the feds and more than three dozen state

and local tax agencies are a sustained "slip through a crack"!).

Here it is in a word:

NOT ONE OF THE

SURRENDERS DOCUMENTED IN THIS SERIES WOULD OR COULD HAPPEN

UNLESS THE FILINGS AND CLAIMS MADE WERE CORRECT AND PROPER UNDER

THE LAW. NOT

ONE. Each of the victories

presented here took place with the knowledge and participation

of tax agency personnel. In almost every case, those victories

took place over and despite the outright resistance of those

officials.

Similarly, NOT ONE of the contortions and evasions

documented in this series would be attempted unless the filings

and claim against which they are deployed is correct and proper

under the law. It is the insurmountably correct character of

these educated filings that compels the tax agencies to resort

to smoke, mirrors and bluster.

Because these things DID and DO happen, the correctness of

CtC-educated filings and claims, and the view of the law on

which they are based, is indisputable.

Enjoy.

|

EVERY WHICH WAY BUT

LOOSE- XII

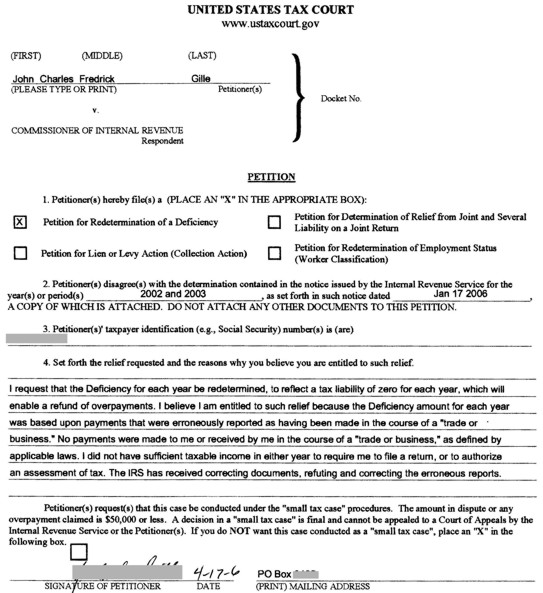

About a year ago I posted the victory of CtC-Warrior

Charles Gille over an IRS effort to disregard his filed

testimony and collect an alleged "deficiency" in

connection with 2002. Charles actually had had two

victories achieved both about the same time, and by way

of the same sequence of events, the other being for

2003-- that's the one we'll add to the story now...

As had been

previously noted in regard to the 2002 victory,

after learning the truth about the "income" tax by

reading CtC, Charles filed amended returns correcting

previously-filed "ignorance tax" returns for 2002 and

2003, rebutting the 1099 "information returns" that

asserted that Charles' earnings for those years were

from taxable activities, and reclaiming the $30 he had

paid-in against what he had previously imagined to be an

outstanding liability. The IRS, hating to see

another American exit the pen, attempted to behave as

though it had the authority to disregard the filings and

calculated proposed "deficiencies", of which it duly

notified Charles, giving him 90 days to contest the

assertion in Tax Court.

Charles did just that:

Shortly afterward, Charles filed an amendment to this

petition, rectifying his misreading of the ridiculously

convoluted "treat as small tax case" election on the

form above, and setting forth his petition with more

specificity. The "service" responded with a

motion to the court to dismiss Charles' petition for

"failure to state a claim upon which relief can be

granted", and seeking the imposition of penalties upon

him for his temerity in challenging the asserted

"deficiency". Charles was instructed by the Tax

Court judge to file another amended petition being more

specific as to his positions. He did-- explaining,

for instance, that:

f. Petitioner had originally reported

receipts and expenses of his sign surveying

business, as though he were an IRC 7701(a)(26)

"trade or business". This error was based upon

Petitioner's ignorance at the time, and his false

belief that the Internal Revenue Service was acting

outside the boundaries of Constitutional law, and

imposing taxes on the inherent right of each human

being to support himself. This was before

Petitioner became aware that the Internal Revenue

laws are carefully designed to require taxes only on

legitimate objects of taxation, such as the type of

activity set forth in the definition of the term

"trade or business" found at 26 USC 7701(a)(26),

that is, some form of government-created or -granted

privilege, which can be properly subjected to an

excise tax, the amount of the tax to be based upon

the income derived from the taxable privileged

activity.

Read Charles' 2nd amended petition here.

Eventually, though, on July 18, 2006, the Tax Court DID

dismiss Charles' petition, while also denying the

penalty sanctions sought by the IRS.

However...

As Charles wrote, describing the subsequent progress of

events over the next two years:

I told the IRS

Commissioner, "OK, fine. I'll be happy to write

you a check immediately, but first, just tell me the

taxable activity that made me liable for an income tax."

He said, "Hmmm. We'll get back to you." Then

I hear from IRS Atlanta, saying I owe the amount that

the auditor said. I tell them the same. They

say, "Hmmm. We'll get back to you." Same

with IRS in Kansas City, Bensalem (PA), Memphis, and

Philadelphia, then a private collection agency, then

back through IRS in Ogden, to the Audit Reconsideration

Unit in Memphis, which had me submit an Audit

Reconsideration form. Then IRS in Holtsville, NY,

says they're working on it, and I should hear by the end

of June. Then nothing until mid-July, when they

send:

Watch out for that robot! I THINK

IT'S GOING TO EXPLODE!!

Isn't it too bad everyone hasn't done like

Charles, and read

CtC-- the exclusive source of the complete,

accurate and liberating truth about the "income"

tax? You can help change that, and thereby

help transform America. Click

here to learn how (while you still can-- see

below...).

|

|

EVERY WHICH WAY BUT

LOOSE- XI

In April of 2008, CtC Warrior Forest Anderson filed an

educated return reporting some interest and dividends

received (all totaling less than the exemption amount),

a modest loss on some other investments, and containing

a rebuttal of a 1099-R which had alleged payments to him

of a considerable amount of "trade or business"-related

deferred earnings. The letter below, which was

attached to his filing, addressed this aspect of the

filing (which can be seen in its entirety

here):

|

April 09, 2008

Department of

the Treasury

Internal Revenue

Service Center

Fresno, CA

93888-0002

Re: TY2007

Return

Dear Sir/Madam:

Please find

enclosed the original filing of my 2007 1040

individual tax return. Please note that I

have enclosed an attached Form 4852, due to the

fact that my payer continues to issue incorrect

and erroneous 1099-R information returns.

My payer has

incorrectly listed payment amounts in 7(B)1 and

7(B)2a. The amounts provided to you by my

payer are in error and in dispute.

Because of the

limited space available on the Form 4852, please

read the enclosed document titled, “My Erroneous

1099-R”.

Sincerely,

Forest L.

Anderson

|

Nearly a year later, in March of 2009, some loose-cannon

scofflaw at the Fresno, California IRS office decided to

test Forest's commitment to the rule of law (or maybe is

just a poor reader...). This law-defier cranked

out a "CP2000" proposing changes to Forest's "account"

to the tune of an $8168.00 liability for 2007, based on

simply disregarding his filing:

Forest wasn't having any... He promptly fired back

with a "No, thanks!":

...and the following letter and enclosures:

|

7008 1140 0004 1952 1900

March 27, 2009

From the desk of:

Forest L. Anderson

XXXXXXXXXXXXXXX

XXXXXXXXXXXXXXX

TIME SENSITIVE: RESPONSE REQUIRED

Department of the Treasury

INTERNAL REVENUE SERVICE

5045 East Butler Avenue

Fresno, CA 93888-0021

Attention: Office of P. Rogers

Letter Number: CP2000

Taxpayer Identification Number

XXXXXXXXXXXXX

RE Tax Form: 1040

Tax Year: December 31, 2007.

Dear Mr. Rogers:

Please place this letter, with the enclosed

documents, in my administrative file.

I

submitted my original TY2007 Form 1040, on

April 10, 2008, by certified mail with

return receipt #7007 0710 0005 5198 8637 to

the Fresno Service Center. My return

included the following documents:

1. Schedule B

2. Schedule D

3. 1 page letter

4. Form 4852

5. My Erroneous 1099-R

6. Notarized Affidavit of Mailing

On April 18, 2008 I received the return

receipt stamped: 2008 April 13 P 5:32 and

received by: “SUBMISSION PROCESSING, IRS,

FRESNO CA.

Wednesday, March 25, 2009, I received the

IRS Notice: CP2000 dated 03-23-2009

(Photocopy enclosed).

Please confirm that you have the above

documents numbered 1-6.

The CP2000 states that I did not include

$2612 in interest in my 1040 return.

That is correct.

However, I did include $2925.22 in interest

on my Schedule B.

I

also included $1741.10 in dividends in part

II of Schedule B.

I

also entered $2925.22 in interest on line 8a

of my 1040.

I

also entered $1741.10 in dividends on line

9a of my 1040.

On the Schedule D Capitol Gains and Losses,

I calculated that I had a Capitol Gain Loss

of $2228.39 and entered -$2228.39 on the

Schedule D.

As instructed, I then entered -$2228.39 on

line 13 of my 1040.

Please read the one page letter I included

with my 2007 return, and My Erroneous

1099-R. Those two documents explain

why I included the IRS designated Form 4852

to correct my erroneous 1099-R.

Thus, I entered 0.00 on line 16b of my 1040.

When these entries were added, my adjusted

gross income was $2437.93. I entered

$2437.93 on line 37 of my 1040 return.

The adjusted gross income of $2437.93 is

clearly less than my standard deduction of

$6650.00.

I

did not omit any interest or

dividends in my return.

I

did correct my erroneous 1099-R.

I

want to thank you for bringing to my

attention a mistake I did make when filing

my 2007 1040. I found that I used the

wrong Form 4852 for 2007. The form had

been changed for 2007 and I used a previous

incorrect form. I have enclosed the

correct 2007 Form 4852.

If the above information clarifies my

2007 return to your satisfaction, thus

eliminating the need of pursuing any further

TY2007 issues and/or issuing further

threatening notices, please do not read

further.

Otherwise please continue:

The CP2000 and an included publication

titled The Examination Process

(Examinations by Mail), inform me, that

my 2007 return has been “examined” and ask

me to agree to the changes that have been

made to my return because of the

examination process. I do not

agree with any of the changes and have

so indicated, in STEP A, OPTION 3, of

the Response Form.

Please permit me to gently inform you of the

law relevant to examinations and summons.

I

have enclosed a document of LEGAL NOTICE and

an AFFIDAVIT OF LEGAL NOTICE with this

letter that relate to your examination

of my records [click

here to see these docs- P. H.].

The document and the accompanying affidavit

puts you on legal notice that I am not

lawfully subject to examination/summons

under the authority reflected at 26 USC 7602

et seq. Any action taken which

purports to apply that authority to me, or

which is in cooperation with an action

purporting to apply that authority to me

which has been initiated by another, is

unlawful, and will be construed as

having been undertaken deliberately and in a

personal capacity. You are

advised to seek competent legal counsel.

I

will further observe, solely for your

edification, that USC Title 26 Section

7214(a) states that:

(a) Unlawful acts of revenue

officers or agents

Any officer or employee of the United States

acting in

connection with any revenue law of the

United States -

(1) who is guilty of any extortion or

willful oppression under

color of law; or

(2) who knowingly demands other or greater

sums than are

authorized by law, or receives any fee,

compensation, or

reward, except as by law prescribed, for the

performance of

any duty; or

(3) who with intent to defeat the

application of any provision

of this title fails to perform any of the

duties of his

office or employment; or

(9) who demands, or accepts, or attempts to

collect, directly

or indirectly as payment or gift, or

otherwise, any sum of

money or other thing of value for the

compromise,

adjustment or settlement of any charge or

complaint for any

violation or alleged violation of law,

except as expressly

authorized by law so to do;

shall be dismissed from office or

discharged from employment and,

upon conviction

thereof, shall be fined not more than

$10,000, or

imprisoned not more

than 5 years, or both. The court may in its

discretion award out

of the fine so imposed an amount, not in

excess of one-half

thereof, for the use of the informer, if

any,

who shall be

ascertained by the judgment of the court.

The court

also shall render

judgment against the said officer or

employee for

the amount of damages

sustained in favor of the party injured, to

be collected by

execution.

Further, each and every penalty that is

imposed without any basis in law and fact,

will be considered an “extortion or willful

oppression under color of law” – a violation

of 26 USC 7214(a) (1).

Further, 18 USC § 872 Extortion by

officers or employees of the United States

Whoever, being an officer, or employee of

the United States or any department or

agency thereof, or representing himself to

be or assuming to act as such, under color

or pretense of office or employment commits

or attempts an act of extortion, shall be

fined under this title or imprisoned not

more than three years, or both; but if the

amount so extorted or demanded does not

exceed $1,000, he shall be fined under this

title or imprisoned not more than one year,

or both.

Further, 18 USC § 876 Mailing

threatening communications

(d) Whoever, with intent to extort from

any person any money or other thing of

value, knowingly so deposits or causes to be

delivered, as aforesaid, any communication,

with or without a name or designating mark

subscribed thereto, addressed to any other

person and containing any threat to injure

the property or reputation of the addressee

or of another, or the reputation of a

deceased person, or any threat to accuse the

addressee or any other person of a crime,

shall be fined under this title or

imprisoned not more than two years, or both.

Please understand that none of these

criminal offenses require that you’re

involved directly and benefit from the

crime. That is to say, extorting

money by threat, etc., is criminal even

if it is only done as the agent of the

direct beneficiary of the extorted money.

Thus, for a government agent to extort

money by threat is a FELONY and

to do so, where the extortion would result

in a financial benefit to the government is

a multiple FELONY.

Further, 26 USC § 6203 Method of

assessment

The assessment shall be made by recording

the liability of the taxpayer in the office

of the Secretary in accordance with rules or

regulations prescribed by the Secretary.

Upon request of the taxpayer, the Secretary

shall furnish the taxpayer a copy of the

record of the assessment.

Further, among the rules or regulations

prescribed by the Secretary, per the

directive reflected at 26 USC § 6203, we

find:

26 CFR § 301.6203-1 Method of assessment

The district director and the director of

the regional service center shall appoint

one or more assessment officers. The

district director shall also appoint

assessment officers in a Service Center

servicing his district. The

assessment shall be made by an assessment

officer signing the summary record of

assessment.

Therefore, I request that the Secretary

furnish me with an actual photocopy of my

record of assessment within 30 days of

the mailing date of this letter, April 17,

2009, with the signature of the assessment

officer included, and an explicit statement

that the reason for the request was both

to establish the existence of the

assessment, and to determine for myself the

assessment’s complete compliance with all

related provisions of law.

The making of this request is not to be

considered or construed as an admission of

“taxpayer” status or of liability for any

tax or penalty, and that the refusal

to cooperate with the request will be

recognized as an acknowledgement that

I am NOT, in fact, liable for the tax or

penalty alleged to be due and owing or

otherwise collectible in any manner on the

Notice: CP2000 received, a copy of

which is enclosed. Please note:

An aggregate record will not satisfy my

request, as compliance requires

documentation sufficient to clearly

establish my personal liability.

Also, please understand that a refusal

to cooperate with my request for a record of

assessment would be a violation of USC

Title 26 Section 7214(a) (3).

My TY2007 Federal return is complete and

correct to my knowledge and belief.

Please refer to the signed jurat on my

TY2007 Form 1040 page 2, and the signed

jurat on my corrected TY2007 Form 4852.

Kind regards,

Forest L. Anderson

Enclosures:

Affidavit of mailing

Notice: CP2000

Response Form

Legal Notice

Affidavit of Legal Notice

The Examination Process (Publication 3498

/page 1)

2007 Form 4852 (corrected)

My Erroneous 1099-R

|

The "service" spluttered a bit by way of reply:

..and then threw in the towel:

Watch out for that robot! I THINK

IT'S GOING TO EXPLODE!!

Isn't it too bad everyone hasn't done like

Forest, and read

CtC-- the exclusive source of the complete,

accurate and liberating truth about the "income"

tax? You can help change that, and thereby

help transform America. Click

here to learn how (while you still can-- see

below...).

|

|

EVERY WHICH WAY BUT

LOOSE- X

In mid-April of 2008, CtC Warrior Stew Grand submitted

an educated return to the federal government concerning

2007, which included rebuttals of "income" allegations

made by a couple of different payers by way of a

1099-MISC and a 1099-R, respectively, and the

calculation and introduction into the record of his

self-assessment of $0.

More than a year later, in late April of 2009, some

loose-cannon scofflaw at the Chamblee, Georgia IRS

office decided to test Stew's commitment to the rule of

law. This law-defier cranked out a "CP2000"

disputing Stew's declared amount of "income" received,

proposing changes to Stew's "account" to the tune of an

$3,341.00 liability for 2007, based on simply

disregarding his filing:

Stew wasn't having any... He promptly fired back

with a "No, thanks!":

|

May

06, 2009

Internal Revenue Service

4900

Buford Highway

Chamblee, GA 39901-0021

Re:

Notice CP2000 for my 2007 return, response form

enclosed

Enclosed please find copies of my 4852 and

1099-MISC corrected forms which show why the

accounting on my 1040 form is correct and I

agree to no changes.

I am

not including any phone numbers as I wish to

have all communications in writing.

Thank

you.

Respectfully,

Stewart G. Grand

|

That's all it took to set the scofflaw back down in his

(or her) place:

Watch out for that robot! I THINK

IT'S GOING TO EXPLODE!!

Isn't it too bad everyone hasn't done like Stew,

and read

CtC-- the exclusive source of the complete,

accurate and liberating truth about the "income"

tax? You can help change that, and thereby

help transform America. Click

here to learn how (while you still can-- see

below...).

|

|

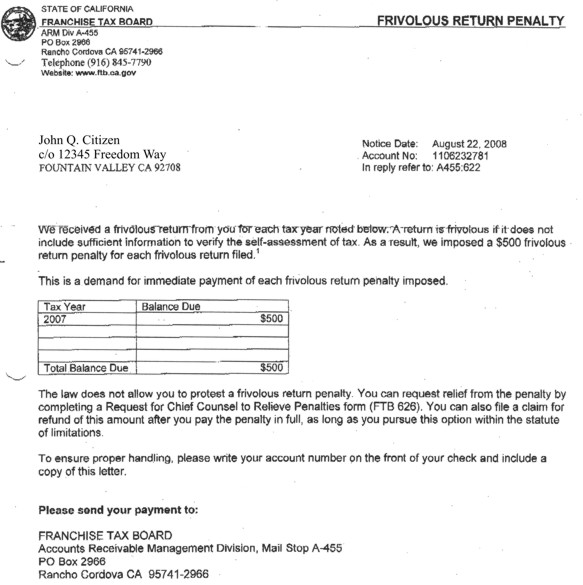

EVERY WHICH WAY BUT

LOOSE- IX

Mabel C. had a little kerfluffle with the California

Franchise Tax Board to deal with recently. It

seems the board wanted to evade the educated return

Mabel and her husband Dave had filed for 2007, in which

Mabel and Dave were reclaiming everything that had been

withheld from her earnings and given over to the state

in connection with the "income" tax.

The board went through the usual motions familiar to

regular EWWBL readers-- declaring Mabel and Dave's

filing to be "frivolous", "assessing" various penalties

and interest, and so forth. All told, the state

tax agency intended to not only keep the $4300.00+ that

Mabel and Dave had claimed for refund, but to take more

than an additional $14K from them:

CtC Warrior Mabel isn't having any of that...

|

Protest Section

Franchise Tax Board

PO

Box 942867

Rancho Cordova, CA 94267-5540

Reference: Notice of proposed assessment dated

05/13/09

Mabel

C.

P. O.

Box

, CA

95

SSN:

Tax

Year: 2007

Proposed assessment amount: 14,331.66

Statements of fact:

a.)

On February 20, 2008 my husband, David , and I

mailed our 2007 joint 540 return. It was

determined that our federal 1040 return was also

needed to complete our return. We

delivered this ahead of the deadline(6/19/2008)

given in the letter dated May 12, 2008.

b.)

As stated in the California Revenue and Taxation

Code, gross income, adjusted gross income, and

taxable income are as defined by IRC sections

61, 62, and 63.

California Revenue and Taxation Code 17071,

17072, 17073:

17071. Section 61 of the Internal Revenue

Code, relating to gross

income defined, shall apply, except as otherwise

provided.

17072. (a) Section 62 of the Internal

Revenue Code, relating to

adjusted gross income defined, shall apply,

except as otherwise

provided. …

17073. (a) Section 63 of the Internal

Revenue Code, relating to

taxable income defined, shall apply, except as

otherwise provided. …

c.)

The amount identified as “CA Taxable Income”

reported by County of Santa Clara is incorrect.

d.)

Federal Adjusted Gross Income(AGI) of $5,392 for

2007 is reflected on line 13 of our California

form 540 return. This amount is taken from

our federal form 1040, line 37. It is

impossible to use a different AGI amount on the

540 than the one calculated and used on a 1040

for the same tax year.

e.)

“State Wages” is given on form 540, line 12, but

is not used in subsequent calculations in

determining the final tax due or tax

overpayment. Relevant calculations use Line 13,

federal AGI.

f.)

The IRS honored our 1040 return for 2007, and on

March 21, 2008 issued the refund due.

g.) I

have one dependent child, Robert, SSN.

h.) I

have deductible items such as Mortgage interest

in the amount of $45,672, and Property taxes in

the amount of $8,891 paid in 2007.

i.)

The assertion that I filed a frivolous return,

for which the subject notice was issued, remains

an unproven allegation. To this date, the

Franchise Tax Board has failed to meet its

burden of proof obligation under Revenue and

Taxation Code section 19180:

19180. (a) In any proceeding involving the

issue of whether or not

any person is liable for a penalty under Section

19177, 19178, or

19179, the burden of proof with respect to that

issue shall be on the

Franchise Tax Board.

I

protest these details of proposed assessment for

the stated reasons:

Regarding “CA Taxable Income”:

“Income”, whether it is “gross”, “adjusted

gross”, or “taxable” is defined in the Internal

Revenue Code as stated in fact “b.”

This holds true for any activity which might be

subject to the income tax. Fact “c.”

applies. At no time during 2007 did I receive

“wages” as an “employee” in a “trade or

business” or any other federally connected

activity. I am submitting California Form

3525 to correct the record with respect to these

facts.

Regarding “standard deduction”:

If I

had engaged in taxable activities during 2007

and were subject to the tax I would itemize

deductions as stated in fact “h.”.

Regarding “Exemptions”:

Please add my dependent child listed in fact

“g.”.

Regarding “Delinquent Return” penalty:

Fact

“a.” demonstrates that I did file a return by

the due date. This penalty has no

foundation.

Regarding the reasons for the issuance of the

notice:

1.)

Having filed a frivolous return:

I

maintain that the return we filed is, to the

best of our knowledge and belief, true, correct,

and complete, or we would not have signed it

under penalties of perjury. Facts “b.”,

“c.”, “d.”, “e.”, and “f.” support our position.

Also of particular value is fact “i”. In a

variety of calls, letters and faxes we stated

our position, asked for clarification, and

expressed our concern that the Franchise Tax

Board has not met its burden of proof, or even

offered details for us to act upon, if we were

actually somehow in error.

2.)

Having failed to respond correctly to the

correspondence of 6/20/08:

The

Frivolous Return Notice dated June 20, 2008

demanded that we file a “valid” return within 30

days. Since we believe our original return

to be correct, we were not inclined to create a

return we would consider to be false. It

is impossible for us to comply with the demand

no matter what the deadline. Given

these facts, the related penalty and this

Proposed Assessment are without foundation.

Finally, regarding the Frivolous Return Notice,

it is addressed to my husband, David. The

Proposed Assessment Notice is addressed to me.

I would appreciate an explanation of this

inconsistency.

Along

with the hearing available to me under the

Revenue and Taxation Code section 19044(a) and

indicated in the FTB 7275 information, I

request and demand any and all due process to

which I am entitled or which is in any way

appropriate and/or available to me under any

provision or practice of common, statutory,

and/or administrative law or protocol.

I

choose to have my husband, David, act as my

authorized representative in these matters.

Under

penalties of perjury, I declare that I have

examined the facts stated in this letter,

including any accompanying documents, and, to

the best of my knowledge and belief, they are

true, correct, and complete.

Sincerely,

Mabel

C.

Daytime phone

David

P. O.

Box

, CA

95

Daytime phone:

Attachments:

Copy

of the Notice of Proposed Assessment

Completed Power of Attorney Declaration.

Form

3525 Substitute for Form W-2

This

three page letter and three attachments were

sent on July 8, 2009 via U.S. Postal Service

Certified mail, tracking number 7008 3230

0002 1951

|

...and the FTB has stopped dishing it out:

Of course, this isn't done, yet. These folks still

owe Mabel and Dave a lot of money...

Watch out for that robot! I THINK

IT'S GOING TO EXPLODE!!

Isn't it too bad everyone hasn't done like

Mabel, and read

CtC-- the exclusive source of the complete,

accurate and liberating truth about the "income"

tax? You can help change that, and thereby

help transform America. Click

here to learn how (while you still can-- see

below...).

|

|

EVERY WHICH WAY BUT

LOOSE- VIII

CtC Warrior Debra Gonzales was subjected to the theft of

her pay by way of an IRS "notice of levy"

beginning in July, 2009, theoretically based on an

existing, valid assessment concerning 2003:

Debra didn't see it that way... After some vain

efforts to get better behavior from the company which

was diverting her property based on nothing more than a

piece of paper, she sent the following demand to

Area 8, Area

Director, Nashville

801 Broadway, MDP1

Nashville, TN 37203

and

Technical Services Advisory Group

401 W. Peachtree St., NW, Stop 333-D

Atlanta, GA 30308

|

Release of Levy/Request for Refund/Attempt to

Exhaust Administrative Remedies

Debra E. Gonzales

XXXXXXXXXXXXXX

Augusta, Georgia 30909

Account #:

September 8, 2009

RE: Demand for Release of Levy/Request for

Refund/Attempt to Exhaust Administrative

Remedies

Attn. Compliance Technical Support Manager or

other Secretary of the Treasury delegate/

Chief, Special Procedures Function

Dear Sir:

I, Debra E. Gonzales, hereinafter Declarant,

state that the facts contained herein are true

and correct and to the best of Declarant’s

firsthand knowledge and belief under penalty of

perjury pursuant to the laws of the United

States of America.

This is Declarant's attempt exhaust

administrative remedies and to comply with 26

USC § 7433(d)(1) and 26 C.F.R. § 301.7433-1, 26

C.F.R. § 301.6343-1(a) & (b)(2).

The grounds upon which Declarant demands that

you issue a certificate of release with respect

to the attached Notice of Levy (which states on

Part 1, "The Internal Revenue Code provides that

there is a lien for the amount

that is owed" (emphasis added)), springs from 26

U.S.C. § 6325(a)(1) & 26 CFR 301.6325-1(a)(1);

in particular, “the entire liability for the

tax…[is] unenforceable as a matter of law”. This

is Declarant's sincere effort to obtain waiver

of sovereign immunity and give herself standing

to sue under 26 U.S.C. § 7433(a),

“In

general,

If, in connection with any collection of Federal

tax with respect to a taxpayer, any officer or

employee of the Internal Revenue Service

recklessly or intentionally, or by reason of

negligence, disregards any provision of this

title, or any regulation promulgated under this

title, such taxpayer may bring a civil action

for damages against the United States in a

district court of the United States."

The property that you are wrongfully levying is

Declarant's earnings from XXXXX of

Dalton,Georgia to for services rendered by her

to XXXXX of Dalton, Georgia. This levy

originated from Kansas City, Missouri. The

date on the notice of levy is July 16, 2009, and

it was received by XXXXX of Dalton, Georgia on

July 29, 2009, who then sent a copy to Declarant

which was received on July 30, 2009. A

copy of the Notice of Levy, which was obtained

from XXXXX of Dalton, Georgia, is attached as

EXIBIT A.

You have ignored 26 USC § 6335 requiring

that you give Declarant post seizure notice by

leaving it at Declarant's "usual place of

abode." You have never done this. An

alternative is given within that statute of

mailing Declarant something at her "last known

address." You have never done that either.

Declarant has suffered the following damages as

a result of your actions: Emotional

distress; economic hardship; physical distress;

embarrassment. Declarant's status with XXXXX of

Dalton, Georgia is in jeopardy because of this

making it look to Declarant's superiors as if

Declarant doesn’t pay her taxes. So far you have

taken $2,000.00+ by way of the levy you have

imposed. Declarant estimates the lost interest,

late fees and emotional distress and

embarrassment damages to be roughly $3,000.00.

Declarant has also delayed a medically necessary

surgery, and will possibly have to cancel it, if

she can not obtain the money to pay her part of

the costs that insurance will not pay, which

Declarant has been told will be

$3,000.00.Declarant has sent a copy of the

letter from her doctor to Ms. Ivory at the

Taxpayer Advocate Office in Atlanta, Georgia.

Further, Declarant contends that the economic

hardship you have caused her by taking the lions

share of her workplace earnings is sufficient

grounds under 26 USC § 6343(a)(1)(D) to release

the levy at XXXXX of Dalton, Georgia.

What follows is the basis for the demand that a

certificate of release respecting the attached

levy issue due to “the entire liability

for the tax…[being] unenforceable as a matter of

law”.

Declarant sent a Freedom of Information Act

(FOIA) request requesting that the Disclosure

Specialist send her, “…a copy of the signed

assessment as promised to me by 26 USC 6203 and

26 CFR § 301.6203-1.” Section 6203 states that,

when requested by a taxpayer, “the Secretary

shall furnish the taxpayer a copy of the record

of assessment.” Treasury Regulation § 301.6203-1

specifies that an assessment is made “by an

assessment officer signing the summary record of

assessment.” A copy of that FOIA request is

attached hereto and incorporated herein by

reference as EXHIBIT B.

In United States v. Merriam, 263 U.S.

179, 188 the Supreme Court said, “It is

elementary that tax laws are to be interpreted

liberally in favor of taxpayers and that words

defining things to be taxed may not be extended

beyond their clear import. Doubts must be

resolved against the Government and in favor of

taxpayers.” Also see Bowers v. N. Y. & Albany

Co., 273 U.S. 346, 350 and Miller v.

Standard Nut, 1932.SCT.40102

<http://www.versuslaw.com> ¶ 35; 284

U.S. 498 (1932). "The legislature must be

presumed to use words in their known and

ordinary signification." Levy's Lessee v.

McCartee, 6 Pet. 102, 110. "The popular or

received import of words furnishes the general

rule for the interpretation of public laws."

Maillard v. Lawrence, 16 How. 251, 261. And

see United States v. Buffalo Gas Co., 172

U.S. 339, 341; United States v. First Nat.

Bank, 234 U.S. 245, 258; Caminetti v.

United States, 242 U.S. 470, 485.

The word “copy” is defined at dictionary.com as,

“An imitation or reproduction of an original; a

duplicate.”

It is not within the province of a court to

modify the law by construction. Crooks v.

Harrelson, 1930.SCT.40822 <http://www.versuslaw.com>

¶ 21; 282 U.S. 55 (1930). It follows then that

it is not within the province of administrative

agencies, as the IRS presents itself to be, to

“modify the law by construction.” When it comes

to taxing acts adherence to the letter applies

with peculiar strictness. Crooks v. Harrelson,

1930.SCT.40822 <http://www.versuslaw.com> ¶ 21;

282 U.S. 55 (1930). The pole star of

interpretation of statutes must be the intention

of Congress, when that can be clearly

ascertained and is reasonably borne out by the

language used. United States v. Stone &

Downer Co., 1927.SCT.40496 <http://www.versuslaw.com>

¶ 93; 274 U.S. 225 (1927). Nearly one

hundred eighty years ago Mr. Justice Story

announced the fundamental doctrine which no

court, or supposed administrative agency should

forget. "Arguments drawn from impolicy or

inconvenience ought here to be of no weight. The

only sound principle is to declare, ita lex

scripta est, to follow, and to obey. Nor, if a

principle so just and conclusive could be

overlooked, could there well be found a more

unsafe guide in practice than mere policy and

convenience." United States v. Stone & Downer

Co., supra @ ¶ 98.

It follows then that when Congress says via 26

U.S.C. § 6203 that, “the Secretary shall furnish

the taxpayer a copy of the record of assessment”

that what they meant Declarant had a right to

was, “An imitation or reproduction of an

original; a duplicate.” It also follows then,

that what the Disclosure Specialist sent

Declarant, in response to her FOIA request,

which is also attached as EXHIBIT C (boldly

titled “Account Transcript”), constitutes a copy

that according to him/her, “… meets all

statutory requirements of Internal Revenue Code

Section 6203 and applicable regulations.”

Treasury Regulation § 301.6203-1 states that an

assessment is made, “…by an assessment officer

signing the summary record of assessment.”

26 U.S.C. § 6322 states, “…the lien imposed by

section 6321 shall arise at the time the

assessment is made…” The procedures set forth in

the Internal Revenue Code were prescribed for

the protection of both Government and taxpayer.

Brafman v. United States, 1967.C05.40183

<http://www.versuslaw.com> ¶ 32; 384 F.2d 863

(5th Cir. 1967). Neglect to comply with those

procedures may entail consequences which the

neglecting party must be prepared to face,

whether such party be the taxpayer or the

Government. Id. In a technical legal sense a tax

does not accrue until it has been assessed and

becomes due. United States v. Anderson,

1926.SCT.40020 <http://www.versuslaw.com> ¶ 56;

269 U.S. 422 (1926).

Declarant has examined IRM Part 25 dealing with

“assessments” here: http://www.irs.gov/irm/part25/ch06s05.html#d0e16308

and the only place Declarant can find any

reference to a “signed assessment is

“25.6.5.10.2 After Hours & Imminent

Assessments” where it says in (2)(E), “Route the

signed assessment document with the case file,

via " Hand carry Mail" , to RACS Accounting

function.” Declarant has also spent quite a bit

of time reviewing the IRM and has not found a

requirement there for an assessment officer to

sign assessments. In Brafman v. United States,

supra @ ¶ 33 the court points out that, “…courts

have not hesitated to enforce strictly the Code

requirement that a taxpayer's returns must be

signed to be effective. Thus, unsigned returns,

even with remittances, have been viewed as

nullities from the standpoint of imposition of

penalties and of commencement of the running of

the statute of limitations. It has availed the

taxpayer little that his failure to sign was

inadvertent.”

In Declarant's FOIA request she asked for, “a

copy of the signed assessment” (emphasis

added) and the Disclosure Specialist responded

with “...an account transcript for tax year 2003

consisting of 2 pages. The account transcript

meets all statutory requirements of Internal

Revenue Code Section 6203 and applicable

regulations.” It is apparent that these copies

do not contain a signature of an assessment

officer meaning that these so called assessments

are nullities and a tax has not been assessed.

If there is no valid, signed assessment, then,

there is no lien arising in the favor of the

United States pursuant to 26 U.S.C. § 6321 and

Declarant is justified on the above basis in

demanding that you issue a certificate of

release of Notice of Levy (which states on Part

1, "The Internal Revenue Code provides that

there is a lien for the amount

that is owed" (emphasis added)), pursuant to 26

U.S.C. § 6325(a)(1) & 26 CFR 301.6325-1(a)(1)

respecting the attached so called levy. (Note:

Declarant has never seen, or been given, any

notice or evidence of the lien mentioned in the

Notice of Levy.)

Declarant therefore demands that a certificate

of release respecting the attached Notice of

Levy (which states on Part 1 "The Internal

Revenue Code provides that there is a lien

for the amount that is owed" (emphasis added)),

issue due to the “the entire liability for the

tax…[being] unenforceable as a matter of law”.

Further, Declarant has received a copy of

documents with “Notice of Levy on Wages, Salary,

and Other Income” on it sent to XXXXX of Dalton,

Georgia pertaining to a “TAX LEVY” in the amount

of $27,367.24. These documents appears to be

sent by the Department of Treasury,

Internal Revenue Service alleging a tax

liability for the year 2003 in an attempt to

levy Declarant's workplace earnings. The EXIBIT

A TAX LEVY instructs XXXXX of Dalton,

Georgia to convert Declarant’s payments

for services to the Department of the Treasury,

Internal Revenue Service. The purpose of

Declarant’s letter is to inform you that it

appears that the Department of Treasury,

Internal Revenue Service has not completed the

prerequisite administrative procedures,

therefore, due process of law is lacking, and

this TAX LEVY is not in full compliance with

Federal law; further, that you, and your

apparently de facto delegate Debra K. Hurst,

Operations Manager, Collections, Kansas City, MO

and/or the “Automated collection system support”

have knowingly ignored Federal Regulations

and Federal Statutes leaving the United States

open to a suit under 26 U.S.C. § 7433 by way of

28 USC § 1346(a) (1) & (e), 28 USC § 1402(c).

Declarant contends that you have done this in

violation of Public Policy and have done so in

order to punish her for what you may possibly

perceive to be a lack of compliance. Declarant

contends that this punishment is in violation of

the United States Supreme Court decision Bell

v. Wollfish, 441 US 520 (1979), in which the

Court held that there could be no punishment

prior to conviction.

26 USC § 7433. Civil damages for certain

unauthorized collection actions:

(a) In general If, in connection

with any collection of Federal tax with

respect to a taxpayer, any officer or

employee of the Internal Revenue Service

recklessly or intentionally, or by

reason of negligence, disregards any

provision of this title, or any

regulation promulgated under this title,

such taxpayer may bring a civil action for

damages against the United States in a

district court of the United States.

The form used for TAX LEVY sent to XXXXX

of Dalton, Georgia by the department of

Treasury, Internal Revenue Service entitled

Notice of Levy on Wages, Salaries, and Other

Income is insufficient on its face as

it merely conveys information, and therefore has

no force or effect of Law. Until all required

procedures have been completed according to

their corresponding regulations as prescribed by

the Secretary, no lawful levy process may

begin. There must be a Judicial Court Order

authorizing the levy when issued against

Declarant’s workplace earnings.

For the purpose of determining the exact point

in time when the law would consider the levy

effective Internal Revenue Code (IRC) section

6502 (b), evidences to wit:

(b) Date when a

levy is considered made. The date on which a

levy on property or right to property is

made shall be the date on which the Notice

of seizure provided in section 6335(a) is

given.

27CFR Part 70.11

Definitions

Seizure: The act

of taking possession of property to satisfy

a tax

liability or by

virtue of an execution.

“Seizure”, as

defined in Black’s Law Dictionary, Abridged

6th Edition, evidences to wit:

The act of taking

possession of property, e.g., for the

violation of law or by virtue of an

execution of a judgment. Term implies a

taking or removal of something from the

possession, actual or constructive, of

another person or persons.

Declarant has not seen any documentation that

her workplace earnings are in the possession of

the Department of Treasury, Internal Revenue

Service. If you have any documentation that this

is the case, please send Declarant the evidence

of such documentation immediately.

Declarant did not receive the notice of

seizure required by law, in violation of

6335(a).

As evidenced above, seizure must have already

taken place. A levy cannot occur without a

seizure. An attempt is being made to

reverse this procedure by using a notice of levy

to accomplish a seizure. This action

violates federal tax laws of USC Title 26.

26 IRC 6335(A), evidences to wit:

Sale of seized property.

Notice of seizure.

As soon as practicable after seizure of

property, notice in writing shall be given

by the Secretary to the owner of the

property...

Property must first be brought into the legal

custody of the United States government before

it can be levied upon, as there must be actual

or constructive physical appropriation of the

property. This is seizure. Mere

intent to reduce to possession and control

through notice is insufficient.

A levy cannot occur until the date on which a

legal, lawful notice of seizure is provided. If

there has been no seizure, there can be no

legal, lawful notice of seizure; therefore,

there can be no levy. The Department of the

Treasury, Internal Revenue Service has no

authority to levy upon any property that is not

already in the Possession of the United States

government.

26 IRC 6331.

Levy and distraint.

(a) Authority of Secretary. (Section (a) has

been eliminated from the notice of levy sent

from you). (Here in part) …Levy may be

made upon the accrued salary or wages of any

officer, employee, or Elected official, of

the United States, the District of Columbia,

or any agency or instrumentality of the

United States or the District of Columbia,

by serving a notice of levy on the employer

(as defined in section 3401(d) of such

officer, employee, or elected official.

The IRS may levy the wages of officers,

employees or government officials because their

wages are already in the possession of the

government, therefore, seizure is perfected.

The Notice of Seizure is therefore provided on

the wages, which are already in possession, and

the levy is perfected. This section (a)

has been omitted from the backside of your copy

of the Notice of Levy. This can be very

misleading as addressed in two separate letters

from two different United States Congressmen

Dennis M. Hertel and E. Clay Shaw, Jr.; a copy

of both letters are attached hereto and

incorporated herein by reference as EXHIBIT D,

which state to wit:

“…Notice of Levy on Wages…Section 6331 IRC

entitled “Levy and Distraint” And Section

6331(a) IRC entitled ‘Authority of Secretary’…does

not provide Authority to levy wages of private

citizens in the private sector. The

Omission of this section from IRS form 668-W may

be misleading to some employers…”

“This particular provision does not appear to

extend to private sector employees. If a form

was given to an employer that omitted section

(a), this form could be considered misleading.”

The limitations of the IRS to levy are pointed

out in their code in sections 7401:

§ 7401.

Authorization

No civil

action for the collection or recovery of taxes,

or of any fine, penalty, or forfeiture, shall be

commenced unless the Secretary authorizes or

sanctions the proceedings and the Attorney

General or his delegate directs that the action

be commenced.

The parallel authorities is in 27 CFR part 70.

27 CFR part 70 has authority under BUREAU OF

ALCOHOL, TOBACCO and FIREARMS.

Declarant is not subject to the authority of

BUREAU OF ALCOHOL, TOBACCO AND FIREARMS, which

is being used against her. Title 26 USC

§ 7403. Action to enforce lien or to subject

property to payment of tax

has the exact same authority as 7401--- 27 CFR

part 70.

Authorization for the collection or recovery of

taxes, etc., is directed through court action

for those who are not under government control

through employment. The result could be

the finding of a person to be a judgment debtor,

resulting in a court order being issued in favor

of the United States. Until a court order

is attained, the Department of Treasury,

Internal Revenue Service has no authority to

impose a levy on anyone who is not a government

official as above. The only persons who can be

levied upon by a TAX LEVY are certain government

officials or others whom the courts have

declared to be judgement debtors by an order of

the court, i.e., by court order. A court

order is necessary for the levy of Declarant’s

workplace earnings.

The Department of the Treasury, Internal Revenue

Service appears to be unlawfully pointing out

the code, omitting certain sections to unaware

employers and other fiduciaries, which seem to

indicate, if they do not comply and levy the

wages of a non-federal employee or non-court

ordered person, they can be sanctioned.

Department of the Treasury, Internal Revenue

Service uses Internal Revenue Code Section

6332(b)(1), which evidences in part:

IRC Sec. 6332. Surrender of property subject

to levy.

Enforcement of levy.

Extent of personal liability. Any

person who fails or refuses to surrender any

property or rights to property, subject to

levy, upon demand by the Secretary, shall be

liable in his own person and estate to the

United States in a sum equal to the value of

the property or rights not so surrendered…

The Department of the Treasury, Internal Revenue

Service fails to inform the same unaware

employer and other Fiduciaries of the law as it

exists in the Code of Federal Regulations

302.6332-1(c)(2), evidencing to wit:

26 CFR 301.6332-1(c)(2)

Any person who mistakenly surrenders to the

United States property or rights to Property

not properly subject to levy is not relieved

from liability to a third Party who owns the

property.

Declarant notes that 26 USC § 6343

provides YOU with authority to release a levy,

and 26 USC § 6343(b)(1)(2) allows for the

return of property wrongfully levied upon.

Based upon the foregoing, Declarant contends

that you have sufficient grounds to do both.

This is Declarant's attempt to exhaust

administrative remedies and to comply with 26

USC § 7433(d)(1) and 26 C.F.R. § 301.7433-1, 26

C.F.R. § 301.6343-1(a) & (b)(2).

Declarant demands that you issue a certificate

of release with respect to the attached Notice

of Levy (which states on Part 1, "The Internal

Revenue Code provides that there is a lien

for the amount that is owed" (emphasis added)),

springs from 26 U.S.C. § 6325(a)(1) & 26 CFR

301.6325-1(a)(1); in particular, “the entire

liability for the tax…[is] unenforceable as a

matter of law.”

Declarant therefore demands that you release the

levy at XXXXX of Dalton, Georgia and return the

funds that you have seized to date.

Thank you for your prompt attention to this

matter.

Sincerely,

Debra E. Gonzales

|

The result?

Way to stand your ground, Debra!

Watch out for that robot! I THINK

IT'S GOING TO EXPLODE!!

Isn't it too bad everyone hasn't done like

Debra, and read

CtC-- the exclusive source of the complete,

accurate and liberating truth about the "income"

tax? You can help change that, and thereby

help transform America. Click

here to learn how (while you still can-- see

below...).

|

|

EVERY WHICH WAY BUT

LOOSE- VII

In early 2007, CtC Warrior G. K. filed an educated

federal return/claim for refund for 2006 and received

all of his withheld property back promptly and without

incident, as expected:

Normally, that would be that, but annoyingly, nearly a

year later some IRS thug decided to take a shot at

scaring G. into repudiating his testimony, abandoning

his self-respect and embracing a lie:

Guess what? G. is a real American-- something this

IRS goon apparently wasn't familiar with...

This set G.'s bureaucratic correspondent back on his

heels a bit; the response was a, "Gee, maybe we'll take

another look at this...":

(I get the image of Jake Blues, after having it pointed

out how much trouble he would have eating

corn-on-the-cob without any teeth, weakly assuring the

band leader he's just tried to shake down that he'd "put

his group on waivers" and straighten things out with Bob

of 'Bob's Country Bunker'...)

Well, the agency DID take another look, and it did

straighten itself out:

Watch out for that robot! I THINK

IT'S GOING TO EXPLODE!!

Isn't it too bad everyone hasn't done like G.,

and read

CtC-- the exclusive source of the complete,

accurate and liberating truth about the "income"

tax? You can help change that, and thereby

help transform America. Click

here to learn how (while you still can-- see

below...).

|

|

EVERY WHICH WAY BUT

LOOSE- VI

In March of 2009, CtC Warrior Susan Blanchard was on the

receiving end of one of those

can-we-invite-you-back-into-the-barn "Proposed Tax

Increase" efforts with which regular readers of this

series are all-too familiar. This one asked Susan

to decide that she really owed Uncle Sammy north of

$24K, rather than "nada", which is what she had already

calculated:

Susan declined...

|

March 4 2009

Internal Revenue Service

Fresno IRS Center

5045 East Butler Avenue

Fresno, CA 92888-0021

RE: Response to Notice

CP2000 – Proposed IRS Changes to 2007 Form

1040

Social Security

Number

531-60-9257

AUR Control Number 50019-3735

To Whom It May Concern:

I received an unsigned Notice

CP2000 (hereinafter referred to as “Notice”)

dated March 2, 2009, a copy of which is

enclosed, that stated in Paragraph 1., Why

are you getting this notice?. “The Income

and payment information (e.g., wages,

miscellaneous income, interest, income tax

withheld, earned income credit, etc.) that

we have on file does not match entries on

your (my) 2007 Form 1040.”

In accordance with the

Noticed, as stated on Page 3, I have

completed Step A, and checked the box marked

“OPTION 3”, I DO NOT AGREE with any

of the changes the Internal Revenue Service

is proposing. The CP2000 proposal to change

the sworn testimony of my valid 2007 Form

1040 tax return. In addition, the IRS has

no lawful authority to change my return.

The information reported to

you about me from , that you reference on

Page 6 in your Notice under the section

‘NONEMPLOYEE COMPENSTATION”, and using it as

your basis to propose changes, is Bad Payer

Data as described in the Internal Revenue

Manual, Part 4.2.2.4.4.(e)

Axxxxx Inc; and Sxxxxx Inc;

are non-governmental, for-profit,

private-sector corporations and/or business

people and have not paid to me any

Federally-connected money for any

Federally-connected service as performed by

me as defined in 26 U.S.C. § 7701(a)(26).

These corporations and individuals(s) have

nothing to do with the performance of the

functions of a public office. There were not

required to report my private-sector payment

on Form 1099-MISC, but did anyway. Of

course, their erroneous information on Form

1099-MISC does not match my correction of

each.

The valid return I

filed for 2007 had documents (signed by me

under penalty of perjury) submitted with it

that corrected the incorrect information

that was reported, and the IRS has processed

them in relation to my return to my

satisfaction in that the “Amount Included on

Your Return” was correctly recorded as $0

(zero dollars). I have enclosed copies

of those documents for your reference and to

support my statement and I will use them in

any court proceeding if needed.

I expect the IRS to

correct its records as to what was reported

to them based on these documents submitted

by me.

If the IRS has firsthand

knowledge of any amounts reported other that

what I have claimed and sworn to under

penalty of perjury. I will require Section

6201(d) verification to support your

position.

No further actions is

required by the IRS or other than to correct

its information (as I have reported the IRS

under penalty of perjury) and respond to me

that this matter is now closed.

I request and demand any and

all due process to which I am entitled or

which is in any way appropriate and/or

available to me under any provision or

practice of common, statutory and/or

administrative law or protocol including,

but not limited to, that to which your

Notice refers; and incorporate by reference

into this request and demand all relevant

information included on or in that Notice or

by requesting and demanding the due process

referenced above.

Be advised that it is my

intention to audio-record any and all

proceedings for which such an options is

lawfully available to me. I declare that I

make no admission as to my status, the

legitimacy of your implicit or explicit

assertions, or the fitness of any particular

legal or administrative protocol by

responding to your Notice or by requesting

and demanding the due process referenced

above.

Prior to any formal or

informal due process hearing, I expect and

require meaningful clarification as to the

nature of and reason for, any alleged

assessment, the process by which any and all

relevant determinations reflected in an by

your office were arrived at, and

anything else pertinent to the matter.

If the IRS or its

officers/agents fail to rebut in writing

within 30 days of receipt of the Response

that with which they disagree, then they

admit to all the above statements as truth

and as fully binding upon them in any court

of the Unites States of America without

protest, objection, or that of those who

represent you.

Under the penalties of

perjury, I declare that I examined the facts

stated in this letter, including any

accompanying documents, ad to the best of my

knowledge and belief; they are true,

correct, and complete.

Thank you,

Susan Blanchard

Encl:

Copy of Notice: CP2000 from

IRS, Notice dated March 02, 2009

2 Corrected Form 1099-MISC

with written statements by me disputing an

correcting incorrect information reported to

the IRS by “PAYEES” referred to above

|

It only took a month and a few days for

satisfaction:

Pretty quick resolution of this abusive little

effort, yes?

Well, actually, it appears that someone over-wound

the Robot on this one, 'cause the very same day that

this closing notice issued, another assault on

Susan's patience began, as evidenced by this:

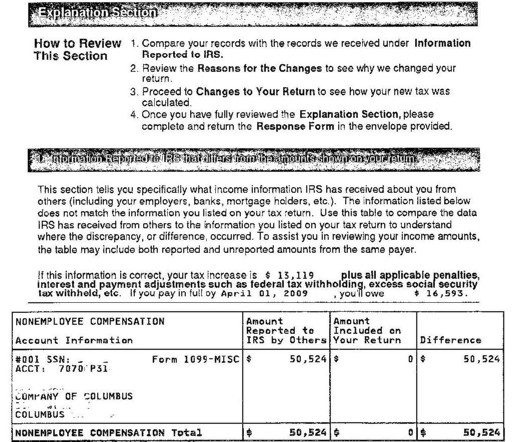

Pretty cryptic, huh? Well, the game being

played here will become clear in a moment, but as we

proceed, I want everyone to remember that the

previous agency docs acknowledge Susan's return--

they refer to it specifically and repeatedly; also,

the IRS had proposed that Susan actually owed

$19,477.00 plus penalties and interest for a total

of $24, 634.00 for 2007.

Now, with both of those things firmly in mind, let's

look at what Susan got next from the IRS concerning

2007:

and

(Note that we've changed IRS offices, here-- the

previous stuff was all from Fresno, California,

whereas the new scary-papers are from Ogden,

Utah...)

Susan quite reasonably shot off a response to these

notices to the same Fresno office with which she had

been dealing in the first place, imagining that it

had lost track of her case. Here is what she

got in reply:

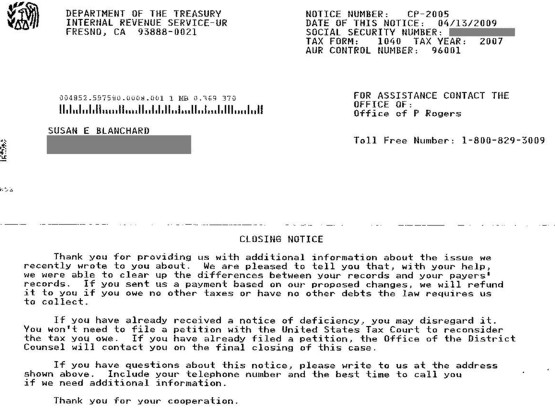

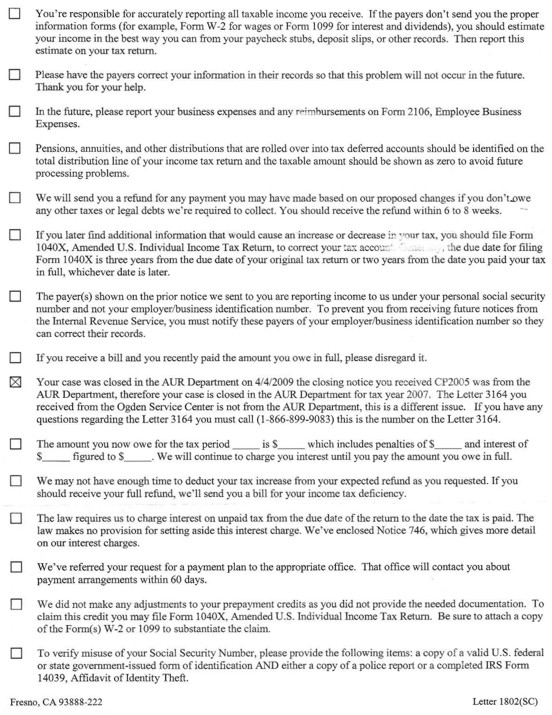

"No mistake", Susan is told-- "we know your case is

closed. This is a different issue..."

Nine days later Susan gets the next level

scary-paper following up on the others-- this time

from... wait for it... the Fresno office! Here

it is:

The Robot is really bouncing and banging, now, but

notice this interesting thing through the smoke and

spraying grease: in addition to the usual weaseling

"assertion" language, and the deliberately

indeterminate "explanation" for the "assertion",

this notice acknowledges that Susan's existing

balance for 2007 is $0.00...

Susan had something to say about this "notice", too:

|

October 14, 2009

Internal Revenue Service

Fresno, CA 93888-001

RE: Notice SP15

dated 09/28/09, Tax Year 2007

Dear Unnamed IRS

Employee:

I disagree with the IRS’

inferred interpretation of IRC 6702 as

pointed out in your notice.

My 2007 Tax Year was

closed on 04\13\2009 as per IRS Notice

CP-2005 – how can you claim a penalty

when I own nothing, and the matter

settled?

At any rate, assessment

has nothing to do with the IRS

determining the amount of “income” on a

return as seems to be inferred in your

quoting of 6702(a) A.1 & 2! It is very

clearly shown via 26 USC 6203 Method of

Assessment:

“The assessment shall be

made by recording the liability of the

taxpayer in the office of the Secretary

in accordance with rules or

regulations prescribed by the Secretary.

Upon request of the taxpayer, the

Secretary shall furnish the taxpayer a

copy of the record of the assessment”

(Boldface added)

And 26 CFR 301.6203-1

that:

“The amount of the

assessment shall, in the case of tax

shown on a return by the taxpayer,

be the amount so shown. . .”

(Boldface, underlining and italics

added)

It doesn’t say, “The

amount of the assessment shall, in the

case of tax greater than zero

shown on a return…” does it? No! If

“taxable income” is “zero”, then the

self-assessed tax amount will naturally

be “zero”. It is inescapable!

You are also inferring

that B.1 or 2. Applies to my return, but

you are leaving it up to me to imagine

which one must be applicable. You

are the party making the accusation, so

surely, you must know which one it is!

However, there is no disclosure in your

notice! I am astounded that you would

think that I would fall for this!

You state toward the end

of the first page that “If you wish to

contest the assertion of

the penalty...” That is an

interesting word to use here: The

American Heritage Dictionary of the

English Language defines “assertion” as:

“A positive statement without support of

proof.” So, what are you doing is making

a statement that I have been charged a

penalty described in a certain section

of law, which is quoted, that you state

I have violated without providing

conclusive proof of same.

Since you are the ones

making the assertion that a “Penalty

Assessment” in the amount of $5,000.00

has been assessed, let’s see it.

Please provide me a copy

of the record of assessment for 2007 as

is allowed by the provisions of 26 USC

6203:

“…Upon request of the

taxpayer, the Secretary shall

furnish the taxpayer a copy of

the record of the assessment…”

(Boldface, underlining added)

within 30 days from the

date of your receipt of this letter as

confirmed by postal return receipt

through the United States Postal

Service.

An aggregate record will

not satisfy this request. Adequate

compliance with this request requires

documentation sufficient to clearly

establish my personal liability. I

demand an actual photocopy, with the

signature of the assessment officer

included. The reason for this request is

both to establish the existence of the

assessment, and of determine for myself

the assessment’s compliance with all

related provisions of the law.

The making of the request

is not to be considered or construed as

an admission of “taxpayer” status or of

liability for any tax penalty. Refusal

to cooperate with this request will be

recognized as an acknowledgement that I

am NOT, in fact liable for the penalty

alleged to be due and owing or otherwise

collectible in any manner as inferred by

your notice!

Emphatically,

Susan Blanchard

CP-2005 Closing Notice

for 2007 Tax Year dated 4\13\09

|

Unfortunately, the Robot wasn't done unwinding.

The next thing Susan received was this (from

Fresno):

and then immediately afterward, this (from Ogden):

Now you see why I drew your attention to the fact

that Susan's 2007 return was long-since

acknowledged-- by Fresno. Maybe it's just not

good enough to send a return to only one IRS office

anymore? Perhaps we all need to pre-emptively

send a copy to every IRS "campus", just to keep

these folks from making silly mistakes (or playing

silly games...)?

Anyway, Susan shot off her replies:

|

November 28, 2009

Department of the Treasury Certified

Mail #: 70051160000 97083543

Internal Revenue Service Return

Receipt Requested

Fresno, CA 93888-0025

Re: CP-504 Notice

Date of notice: 11-27-2009

Dear Internal Revenue Service:

THIS LETTER CONSTITUTES CONSTRUCTIVE

NOTICE OF FACTS TO THE IRS.

I received a ‘CP504’ on 11-02-2009. The

letter contains no authorized name or

signature. The ‘current balance’ and

‘interest’ amounts are erroneous and

invalid. I do not owe any ‘balance due’

nor any tax or penalty liability

whatsoever.

Attached is my IRSs CP-2005

closing Notice dated: 04\13\09 tax for

2007

Please update your 2007 records, thank

you for your prompt action.

Sincerely,

Susan Blanchard

Enc: CP-2005 for TX YR 2007

|

|

November 28, 2009

Department of the Treasury

Certified Mail #: 7005 1160 0001 9708 3642

Internal Revenue Service Return Receipt

Requested

1973 North Rulon White Blvd.

Ogden, UT 84404-0040

Re: Response to Letter 1862

To Ms Love (Employee

Identification Number: 0469241048)

I received your Letter 1862,

and Form 4549 –I have received these in

error – I think your dueling computers are

up to their tricks, in not knowing what the

other computers are doing.

Attached is my IRSs

CP-2005 closing Notice dated: 04\13\09 tax

for 2007

Please update your 2007

records, thank you for your prompt action.

Sincerely,

Susan Blanchard

Enc: CP-2005 for TX YR 2007

|

Now she waits to see what she'll get next concerning

2007 (and from where). In the meantime,

Watch out for that robot! I THINK

IT'S GOING TO EXPLODE!!

Isn't it too bad everyone hasn't done like

Susan, and read

CtC-- the exclusive source of the complete,

accurate and liberating truth about the "income"

tax? You can help change that, and thereby

help transform America. Click

here to learn how (while you still can-- see

below...).

|

|

EVERY WHICH WAY BUT

LOOSE- V

In March of 2009, CtC Warrior Michael was on the

receiving end of one of those

can-we-invite-you-back-into-the-barn "Proposed Tax

Increase" efforts with which regular readers of this

series are all-too familiar. This one asked

Michael to decide that he really owed Uncle Sammy north

of $16K in connection with his earnings during 2007,

rather than the "zero" he had already calculated:

Michael wasn't having any of it...

It only took a month and a few days for

satisfaction:

Watch out for that robot! I THINK

IT'S GOING TO EXPLODE!!

Isn't it too bad everyone hasn't done like

Michael, and read

CtC-- the exclusive source of the complete,

accurate and liberating truth about the "income"

tax? You can help change that, and thereby

help transform America. Click

here to learn how (while you still can-- see

below...).

|

|

EVERY WHICH WAY BUT

LOOSE- IV

In May of 2007, CtC Warriors Joan and Lowell Thompson

were faced with a bluster and bs attack by the IRS,

which sought to intimidate these good Americans into

perjuring themselves and declaring their

non-federally-connected receipts to be so connected, and

therefore taxable as "income", even after

their testimony to the contrary had already been

filed:

Joan and Lowell, firm in their commitment to the rule of

law, stood fast:

Lowell and Joan were treated to another effort a

month-and-a-half later (unfortunately not preserved

to share here), and again responded with firmness

and confidence:

It took nearly a year, but eventually Joan and

Lowell got the "surrender" by the agency to which

they were entitled (and in a form we've not seen

before):

It'd be nice if these bureaucrats would just forget

about all these shameful ploys as soon as they

recognize that they're dealing with

CtC-educated Americans, instead of clinging to

the hope that maybe they've stumbled upon the odd

one or two that might let themselves be intimidated

into collapse, wouldn't it?

Someday...

In the meantime, though,

Watch out for that robot! I THINK

IT'S GOING TO EXPLODE!!

By the way, this isn't the only time

Lowell and Joan have had to deal with

this nonsense. They had the same

ridiculous ploy tried on them the next

year as well, this time for 2006.

See how THAT went on

page 28 of the ever-growing

Victories collection.

Isn't it too bad everyone hasn't done like Joan

and Lowell, and read

CtC-- the exclusive source of the complete,

accurate and liberating truth about the "income"

tax? You can help change that, and thereby

help transform America. Click

here to learn how (while you still can-- see

below...).

|

|

EVERY WHICH WAY BUT

LOOSE- III

This past January, CtC Warrior Vince Smith wasted no

time sending in his claim for the return of everything

that had been withheld from him and given over to the

federal government in connection with the "income" tax

during 2009:

Annoyingly, the IRS wasn't quite as eager to abide by

the law...

(This image combines both pages of

this "LTR 12C" balk-instrument)

However, Vince takes the law seriously, and knows

that it is HIS responsibility to enforce the law

when those in positions of authority and public

trust seek to evade it:

This time the errant agency got the message that

it's dealing with a real American, who won't let

himself be browbeaten, fooled or frightened into

assuming a prone position in the face of government

misbehavior:

It'd be nice if these bureaucrats would just forget

about all these shameful ploys as soon as they

recognize that they're dealing with

CtC-educated Americans, instead of clinging to

the hope that maybe they've stumbled upon the odd

one or two that might let themselves be intimidated

into collapse, wouldn't it?

Someday...

In the meantime, though,

Watch out for that robot! I THINK

IT'S GOING TO EXPLODE!!

Isn't it too bad everyone hasn't done like

Vince, and read

CtC-- the exclusive source of the complete,