|

More Victories For The Rule Of Law- Page Sixty

Hundreds of thousands of readers of 'Cracking the Code- The Fascinating Truth About Taxation In America' have taken control of their own resources, in accordance with, and respect for, the law. The total amount reclaimed by these good Americans so far is upward of several billion dollars.

A few of these good American men and women-- such as those honored below-- are generous enough to send me the evidence of their victories in upholding the law, for the edification and inspiration of everyone. Daniel & Jane Moore

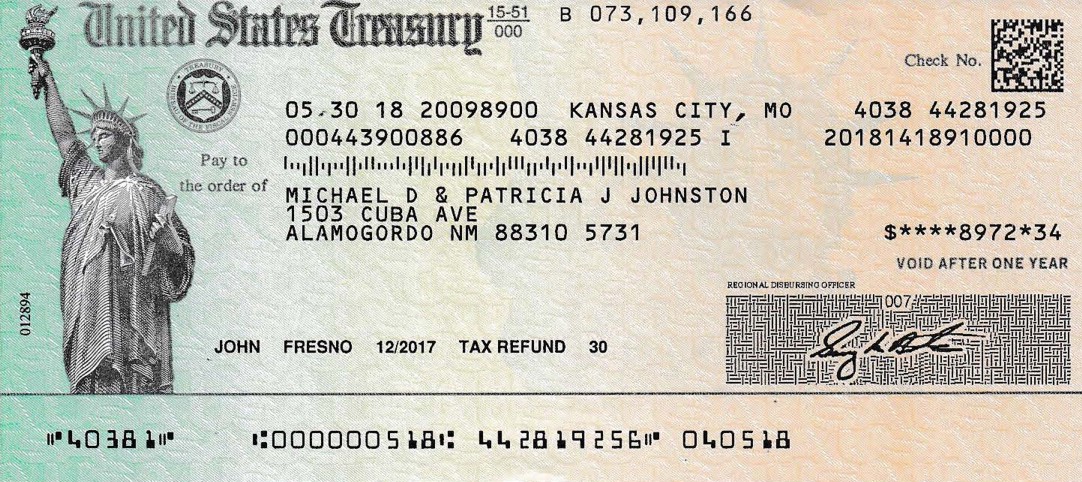

Here is the filing that produced this heartwarming, law-abiding, rapid and no-fuss $34K+ return of Daniel and Jane's property. Michael & Patricia Johnston

This excellent 100%, no-fuss refund came on this filing and claim. Ruben in Fullerton

Although made to look rather not like a victory by the big "amount due" number, the smaller text tells the tale. This is a complete, 100% refund of everything withheld from Ruben during 2017, per his filing and claim. What's more, this is a victory all the more telling for the fact that Ruben is plainly not someone unknown to the IRS, as shown by the large pre-discovery-of-CtC liability to which his acknowledged overpayment was diverted. R. Perez

Here is the return that secured this victory for the rule of law. Paula Seychel PAULA shares one of those especially sweet CtC events-- a reach back years into the past to recover property that never should have been taken. Here is Paula Seychel's complete refund of everything withheld from her during 2014:

This recovery was secured with a CtC-educated return filed in September of 2017.

Joe H. JOE'S filing is as simple an affair as it is possible to get: a 1040 EZ and a single Form 4852 rebutting an errant W-2. That W-2 was created by the company which paid Joe for his labor during 2017 and which withheld a total of $13,511.00, as reported by Joe on his sworn docs. That withholding consisted of $7,728.00 withheld as nominal "federal income tax" (under the provisions of chapter 24 of the IRC) and $5,783.00 withheld as Social security and Medicare taxes (FICA taxes) under the provisions of chapter 21. Here is how the IRS has responded to Joe, so far:

Notice, the agency is proposing a tax liability (we'll get to that in a moment). Against that proposed (we'll get to that in a moment) liability it is acknowledging a credit of everything withheld as nominal "federal income tax"-- that is, the total withheld under the provisions of chapter 24 of the IRC. NOW LET'S LOOK at what the tax agency says about how it arrived at the proposal above. Here is its table of purported calculations...

...and here is its purported explanation of its figures:

What is notable about these assertions to begin with is that all of the explanations attempt to characterize the IRS proposed changes (we'll get to that) as being math errors, or transcription errors, or are pure, unadulterated bs. For instance, the first item alleges that the 1040EZ line 4 AGI was changed "to include all the forms W-2, W-2G, etc. that were attached to your form 1040EZ because there was an error in the total income reported", implying that Joe had not transcribed the "income" amounts reported on his attached forms accurately. But the only form attached to Joe's 1040EZ was his Form 4852. That form reports $0 "wages", a figure accurately transcribed to Joe's 1040 line 1, and resulting in a line 4 AGI total of $0. Pure bs. The next entry is just as much complete, unmistakable horse-hockey. "We changed the amount of taxable income on line 6 of your Form 1040EZ because the combined standard deduction/exemption amount on line 5 was subtracted incorrectly from the adjusted gross income on line 4." Really?! Here is that portion of Joe's 1040EZ:

While it's true that Joe mistakenly checked a "dependent" box in the line 5 instruction, IT DOESN'T MAKE ANY DIFFERENCE! No matter what the proper line 5 amount might have been, line 6 still ends up as $0. The IRS did not change "the amount of taxable income" on Joe's 1040EZ because of his incorrectly subtracting the combined standard deduction/exemption. Pure bs. The third item is the same: pure bs. The amount withheld was not changed to reflect the amounts shown on supporting documents-- the sole supporting document was Joe's Form 4852, and the amount of withholding shown on his return is an exact transcription therefrom. The fourth item is yet another bit of nonsense-- Joe never provided information in response to a correspondence or otherwise which contradicted or called into question amount owed or the refund amount claimed on his return. BUT HERE'S HOW THIS ALL SORTS ITSELF OUT (in a manner of speaking): this apparent disregard of the realities of Joe's filing is just a "prosal". The fact is, all this nonsense by the tax agency, consisting as it does of much huffery and puffery, ends up being nothing but an invitation to Joe to stand down and get back in the "ignorance tax" barn. Here is the second page of the CP11 Joe received: Joe is gratuitously threatened with the possibility of an "audit" if he dares to disagree and the agency doesn't like the "additional information" justifying the abandonment of this proposal, of course. Obviously the agency wants him to just stand down and shut up. But a threat of a possibility is nothing more than that, in the first place; and in the second, the only "additional information" that should be needed to justify the abandonment of this absurd proposal is a brief letter pointing out the bs behind every "explanatory" rationale for the proposed changes. ALL IN ALL, JOE H.'S 2017 victory-in-progress-- in which the IRS just invites Joe to be confused and taken in by a pile of convoluted nonsense-- is a great testament to the truth about the tax revealed in CtC. The tax agency would never in a million years resort to this kind of smoke-and-mirror eyewash unless this was the best it had. And this can only be the best it has because Joe, informed by CtC, is unassailably right in his filing and his claims. But, Watch out for that robot! I think it's going to explode!!

Robert Woolard ROBERT IS A YOUNG MAN just a few years into the working and earning world, and he has gotten off to a proper start. On the same day last week Robert secured a complete refund of everything withheld from him and given over to the feds for income taxes during 2016 and 2017 (including both the normal tax and Social security and Medicare surtaxes), plus interest in each case. Here is Robert's 2016 refund:

Here is the filing by which this refund was secured. (This refund was delayed due to a mistake, at first go-round, in Robert's Social security number entry on his 1040; and isn't it nice to think of a young American who HASN'T got that number tattooed on the inside of his forehead, like so many older Americans do after years of having the thing demanded from us every time we seemingly do anything?). Here is Robert's 2017 refund:

Here is the filing that secured this refund. Well done, Robert, and WELCOME!! RICK IS A VETERAN WARRIOR and long-time true and active American patriot. Today Rick shares his latest pair of educated refunds-- both Federal and state for 2017:

...from this filing; and:

...from this filing. Ray Park AS IS TRUE OF EACH of the next three victories we're going to salute, Ray hasn't yet submitted the filing that produced his 2017 refund:

Ray's check image came to me by snail-mail, along with a note saying, "Dear Pete, After years of bull shit excuses, they finally gave in to the power of the law. Please post. Good to hear your wife has been released! Ray" I've been unsuccessful at contacting Ray by email, so it is my hope that he will see this and reach out to me again, this time with the filing that produced this victory. James in Connecticut

The story here is the same as Ray Park's-- a snail-mail delivery and no way of my following up to ask for the filing docs, which were not enclosed. My message to this fine American is the same-- Congratulations!!! And if you see this please send those docs!! Paul B. ONE MORE WITHOUT THE FILING (so far), but this one is a bit different. Paul is a veteran warrior, and does get my emails. In this case, however, the scans of the filing are on a hard drive which is at the moment not accessible. In what I expect will be the not-too-distant future I will be supplementing this post with the filing associated with this refund:

But in this case there are some documents to share, even though the filing is unavailable at the moment. As will be noted, this refund is for the year 2013, even though issued in March of 2018. Paul filed for this refund quite a while ago, as shown by the nearly $600.00 in interest. But though the United States has acknowledged that Paul is entitled to the return of most of what was withheld from him, and has agreed with everything on his filing related to the amount of "income" received, and tax owed, it is nonetheless trying to get Paul to agree to forego the return of what was withheld from him as "FICA" surtax withholdings (for no particular reason except the government's hope that he will consider the difference not worth arguing about, apparently). A very similar proposal, but with the filing available for examination and clarification, will be discussed below. Here are the relevant portions of the proposal Paul received from the IRS last autumn:

Paul receives a military pension, and thus does have a fair chunk of "income" on which he owes taxes, as shown here. What is errant is the IRS falsification of the amount withheld from Paul, in total. As noted, in the victory post that follows, we will look at the same sort of ploy, and so will say no more about Paul's case here. I'll only note further that while the 9/11/17 notice above tells Paul to expect his check within 4-6 weeks, it wasn't until 6 months later that the thing arrived. Perhaps this is because Paul expressed his refusal to accept this IRS proposal, resulting in this stall letter in December asking for 45 days to consider his answer, which became more than 90 before the check arrived, but still without an answer. Vincent T. MR. T. IS ALSO A VETERAN CtC WARRIOR, with many victories under his belt. Some of Vincent's more recent wins have been of the especially-revealing nuanced variety, and this latest one being shared-- federal for 2017-- falls squarely into that category:

As seen, the IRS is proposing, and asking Vincent to agree, that he made a "miscalculation" on his 1040, which can be seen here. The agency is inviting Vincent to agree that his inclusion of the FICA withholdings on his refund claim was improper. And that inclusion WOULD be improper, IF Vincent had received a sufficient amount of the "wages" which measure the taxable activities upon which FICA tax liability can arise. But he hadn't, and even the IRS admits this:

Note in the "tax calculations" portion of this second page from Vincent's refund proposal notice that the IRS agrees with Vincent's tax return-reported conclusions that he had no AGI, no "taxable income", and owes no tax. A look at Vincent's return will show that the agency is agreeing that Vincent is entitled to every penny of what was withheld from him under the Chapter 24 "normal income tax" withholding provisions-- that's the $7,532.00 it is offering Vincent to accept and then walk away. That is, the agency is agreeing that Vincent had no Chapter 24 "wages" which measure the taxable activity upon which liability for the normal tax arises, just as Vincent says on his return. But because this is so, Vincent is also entitled to the return of every penny of the amounts withheld under the provisions of Chapter 21-- the "FICA" surtax withholdings, since the taxable activities that give rise to both Chapter 24 "wages" are the same as those that give rise to the Chapter 21 "wages". The only distinction between the application of the "normal" tax and the FICA surtax is that the surtax only applies to the first $127,200 received as tax-relevant "wages". Since Vincent received no such "wages", as the IRS plainly agrees both explicitly in its statement above and implicitly by agreeing that Vincent is entitled to the return of all Chapter 24 withholdings, Vincent cannot be liable for any of the Chapter 21 surtaxes, either. OBVIOUSLY, VINCENT WILL HAVE TO OVERCOME the IRS effort to steal his FICA-withheld money (or at least to browbeat or intimidate him into agreeing that the United States is, for some reason entitled to that money). Indeed, that process has already begun. A month before this proposed settlement was floated to Vincent by the IRS, the agency engaged in the pretense of not understanding Vincent's entries on the Forms 4852 with which he rebuts ignorant payer allegations that his receipts constituted "wages". Vincent responded very clearly, articulating exactly what his return is all about, and the IRS response was the agreement of no "income" received, and no tax owed. Here are the docs in that exchange. TThe agency then fell back to the pretenses shown on the document above in the section labeled, "Information was changed because of the following:" in which two false statements are made, 1. that the exclusion of amounts withheld from Vincent under the FICA provisions from the total amount acknowledged as withheld was based on the return's supporting documents (which is to say, the Forms 4852, making this statement absurd); and 2. that the refund amount the IRS is proposing is based on the information Vincent provided in the earlier exchange (documented above). But the agency has already made all the admissions needed for the completion of Vincent's victory in due course. At the same time, the agency has expressly and in every possible way acknowledged the absolute correctness and accuracy of the legal points underlying Vincent's refund claim. Even while it still struggles to get away with misbehavior Vincent has pushed the agency into a very tight corner with his CtC-educated filing and his stalwart and steadfast standing of his ground, just as is the case with Paul B. discussed previously. Well done, Vincent, and well done, Paul!! But, Watch out for that robot! I think it's going to explode!!

This complete (FICA and all) refund is from a filing with both 4852 and 1099-rebuttals and which was heavily-vetted (with not only the usual gauntlet but also pre-issuance challenges to the withholding claimed and to the claimants' identities):

Stephen and Isabelle's victory in upholding the law is an especially-compelling illustration of the fact that the United States knows and quietly admits that what is revealed in 'Cracking the Code- The Fascinating Truth About Taxation In America' (CtC) is the truth about the income tax in America.

Click here to return to the Bulletin Board

Even in the face of the requirements of the law, the junkyard dog still tries to play its losing hand occasionally. Ironically, it is these sporadic spasms of resistance that offer the most telling evidence of the truth about the tax...

Despite the fact that those whose victories are on display here did nothing but insist that the law be applied as it is written, they did so in the face of fearful threats and cunning disinformation from the beneficiaries of corruption. Their actions took great courage and commitment, and I salute them all.

“God grants liberty only to those who love it, and are always ready to guard and defend it.”

-Daniel Webster

NOTE: Whether any given individual is entitled to a refund depends on a number of different factors, and no one should presume that they are so entitled simply because they see that others are. Each person should educate himself or herself about the particulars of the law, and make his or her own determination in this regard.

To get on the Lost Horizons mailing list, send an email to SubscribeMe 'at' losthorizons.com with your name in the message field.

NOTE: The documents displayed on this and any linked pages, and any associated comments, are posted with the permission and cooperation of the upstanding Americans with whom they are concerned. When a return is posted in connection with any refund or other responsive document, it is complete-- that is, what is posted is EVERYTHING filed as a return in connection with that refund or document, unless otherwise indicated. |

{kind=link}