|

More Victories For The Rule Of Law- Page Forty-Nine

Tens of thousands of readers of 'Cracking the Code- The Fascinating Truth About Taxation In America' have taken control of their own resources, in accordance with, and respect for, the law. The likely total amount reclaimed by these good Americans so far is upward of several billion dollars. A few of these good American men and women-- such as those honored below-- are generous enough to send me the evidence of their victories in upholding the law, for the edification and inspiration of everyone. At the moment those shared refund checks, closing notices, and so forth total:

Eric Howarth

The return producing this 2011 victory can be seen here.

This one's for 2012

Larry _

2012

Larry's federal victory for 2012 can be seen elsewhere on these pages

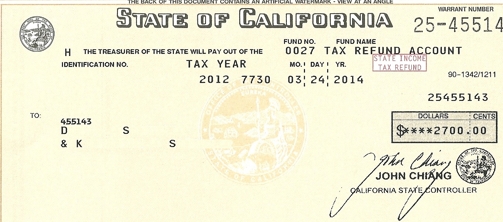

D. & K. S.

2012

D. & K. S.'s federal victory for 2009 can be seen elsewhere on these pages.

Barry Sullivan Barry filed a "conventional" original federal income tax return concerning 2011, reporting all the money that had come in to him during 2011 as "income"-- a $28,000 inheritance from what had been saved as a parent's IRA, and $15,550 that he had earned working. He followed the instructions on the form and ended up calculating a $4,364 tax liability on these amounts he had assumed were subject to the tax, and was reporting as such. Unfortunately, Barry didn't have the money and had only had $182 withheld from his pay as nominal "federal income tax". Crediting him nothing for the federal income tax pre-payments denominated as "Social Security and Medicare taxes", which Barry didn't know to claim in any event, just as he then didn't know to point out that he had no liability for the work-gains in connection with which those amounts were withheld, the IRS calculated an outstanding tax liability for Barry of $4,312.38 as of July 5, 2012:

Barry entered into a payment plan agreement, and started chunking out his hard-earned money to pay this amount. By February of 2014, he had paid the liability down to $2,910.54 (after additional accumulated penalty and interest amounts):

But then Barry learned the truth about the tax, and on March 1, 2014, rather than send in the $150 demanded by the IRS, Barry instead sent in a 1040X amending his original "ignorance-tax" return. Barry calculated a new liability of only $1,851-- this being on only the IRA payout, which Barry treated as taxable on the amended filing. Against this was now the TOTAL amount of $1,060 withheld from Barry from his work-earnings, Social security and Medicare taxes included, plus what Barry had paid in installments. The result of Barry's amended filing was just what it should be and usually is without quibbling or complaint-- a prompt and complete agreement with all of his conclusions. Barry's tax liability is reduced by $2,513 due to his pay being entirely non-taxable, and his credit against the undisputed liability for the IRA funds he inherited going up $878-- every penny of what was withheld from him as Social security and Medicare taxes on that pay:

BY THE WAY, the same day Barry filed his amended return concerning 2011, he also filed his educated original return for 2013. This one contained not just a 4852 rebutting an erroneous W-2 but also two 1099 rebuttals. See that return package here. The result of this 2013 filing and claim? Just as with Barry's simultaneously-filed educated amendment, this filing concerning 2013 produced a prompt, complete agreement with Barry's conclusions and the refund of everything withheld (other than $3 due to an apparent typo-- $619.98 was withheld but it was transcribed to the 1040 as $616.98)-- all of which consisted of Social Security and Medicare withholdings:

Jake

Joseph Davis

Here's the filing that produced this full-credit victory

Here's the filing that produced this full-credit victory.

Guy and Sherrie Placencio

Here are the docs Guy and Sherrie filed to secure this refund , including their response to a sleazy IRS effort to frighten them into reversing themselves by way of a suggestion that their 4852s weren't good enough evidence of what had been paid in "wages" and what had been withheld.

Thomas E.

Tom's filing which produced this victory on behalf of the rule of law and for The People's meaningful discipline of their public servants can be seen here.

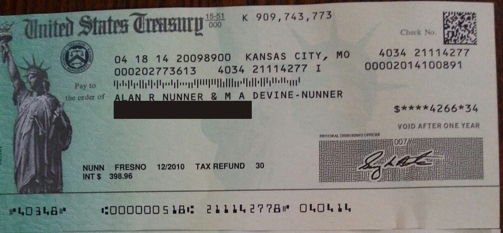

Alan and M.A. Nunner

Paul Anderson

This refund is entirely of FICA withholdings (Social security and Medicare), which is all that had been withheld from Paul during 2013. It was produced by the operation of this filing.

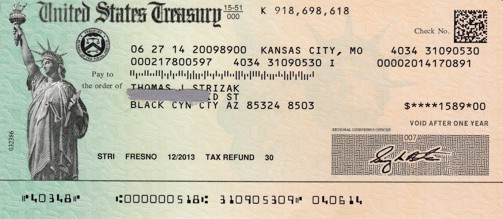

Thomas Strizak

Here's the return filed to secure this Arizona refund of 2013 withholdings; it was accompanied by relevant rebuttal instruments which will be found in the filing that produced this complete federal 2013 refund a month-and-a-half later:

By the way, it will be noted that in addition to a lot of forms 4852, Thomas's filing involved a rebuttal of one of the new 1009-K information returns (discussed here). This is the first educated filing of which I am aware involving one of these new versions of the 1099, and the credit-card "income" allegations it is designed to make.

Jim Whelan

This refund for 2012 (with interest) resulted from this filing, in which, as Jim explains, the FICA withholding was not claimed, simply by mistake. Jim didn't make that mistake with his next claim-- of everything withheld during 2010 (plus interest), by way of an amended filing:

Dennis G.

Dennis secured this refund for 2012 (with interest) by way of this filing, in which, as you will note, he claims everything withheld, while only receiving back the amounts withheld under the label "federal income tax" and not the FICA withholdings. Dennis's response to that incoherent omission-- remember, by its refund, the government has acknowledged that Dennis received no tax-related "wages" by which FICA taxes are measured-- can be seen as the last page of the filed docs.

Click here to return to the Bulletin Board

Even in the face of the requirements of the law, the junkyard dog still tries to play its losing hand occasionally. Ironically, it is these sporadic spasms of resistance that offer the most telling evidence of the truth about the tax...

Despite the fact that those whose victories are on display here did nothing but insist that the law be applied as it is written, they did so in the face of fearful threats and cunning disinformation from the beneficiaries of corruption. Their actions took great courage and commitment, and I salute them all.

“God grants liberty only to those who love it, and are always ready to guard and defend it.”

-Daniel Webster

NOTE: Whether any given individual is entitled to a refund depends on a number of different factors, and no one should presume that they are so entitled simply because they see that others are. Each person should educate himself or herself about the particulars of the law, and make his or her own determination in this regard.

To get on the Lost Horizons mailing list, send an email to SubscribeMe 'at' losthorizons.com with your name in the message field.

NOTE: The documents displayed on this and any linked pages, and any associated comments, are posted with the permission and cooperation of the upstanding Americans with whom they are concerned. When a return is posted in connection with any refund or other responsive document, it is complete-- that is, what is posted is EVERYTHING filed as a return in connection with that refund or document, unless otherwise indicated. |