|

More Victories For The Rule Of Law- Page Fifty-Six

Hundreds of thousands of readers of 'Cracking the Code- The Fascinating Truth About Taxation In America' have taken control of their own resources, in accordance with, and respect for, the law. The total amount reclaimed by these good Americans so far is upward of several billion dollars.

A few of these good American men and women-- such as those honored below-- are generous enough to send me the evidence of their victories in upholding the law, for the edification and inspiration of everyone.

Brandon Little

Here is the filing that produced this admission and refund.

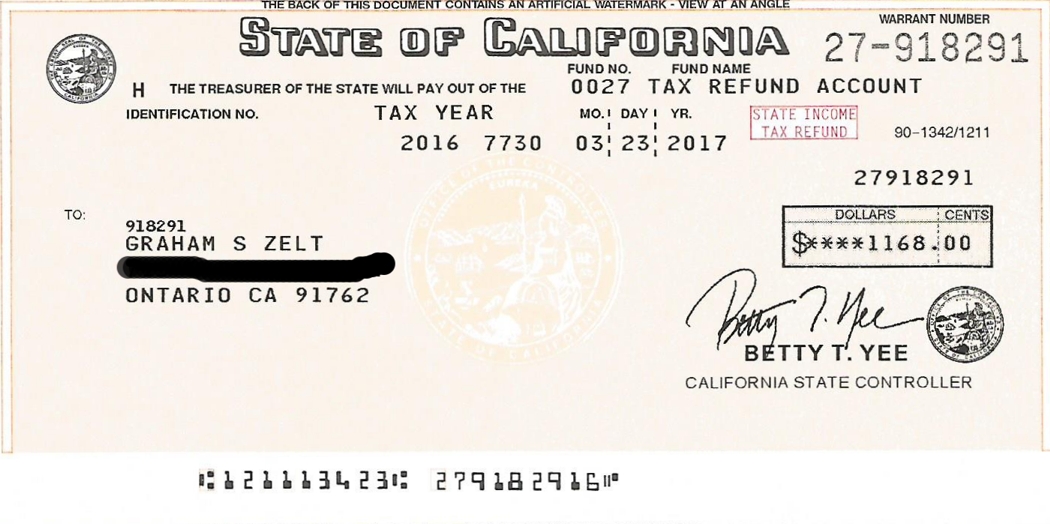

...and here is Graham's claim. Erik Clark

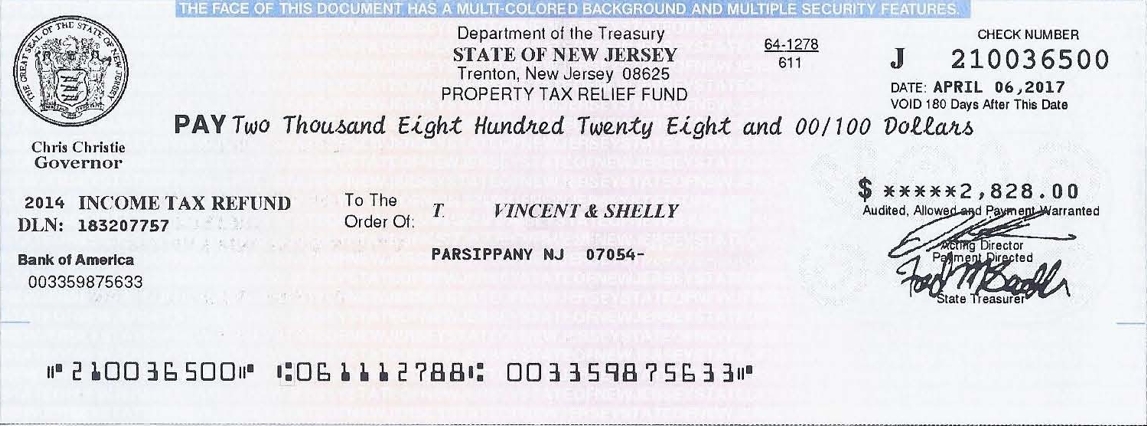

Erik's return can be seen here. Vincent & Shelly T.

Click here to see the amended return which produced this victory. David Custer

Here are the docs filed by David which compelled the United States to abandon the "ignorance tax" scheme in David's case and abide by the law as written (after a bit of initial balkiness by the IRS). Steven Tilden

Here are the docs filed by Steven which compelled the United States to abandon trying to run the "ignorance tax" game on him and instead face the facts and abide by the law as written. Richard A.

Here is the claim Richard submitted that produced this victory for the rule of law. Kara Meldrum

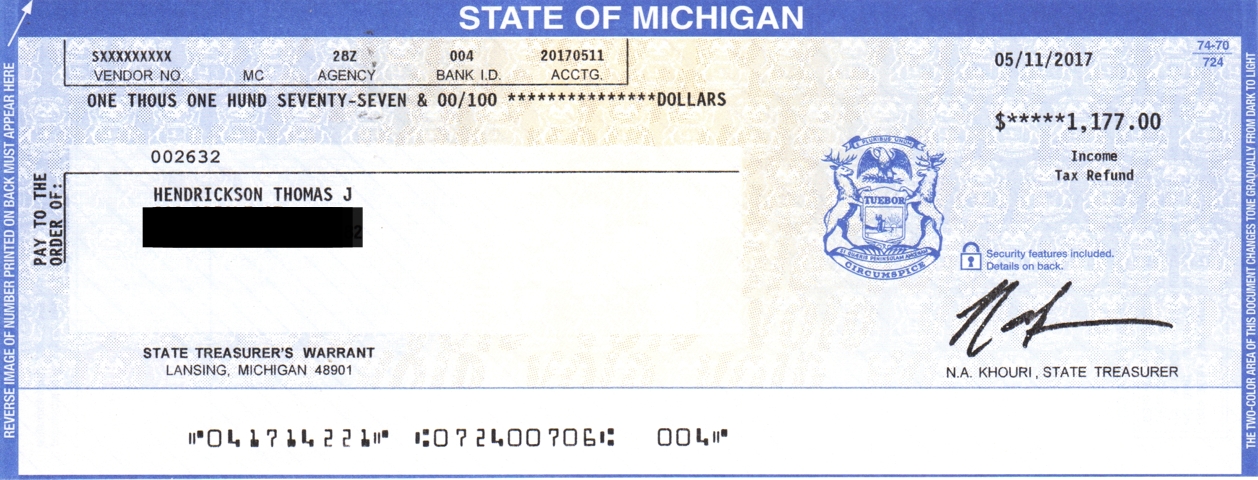

Here is Kara's claim for the return of all her property, it having been determined that none of her earnings qualify as "income" relevant to the tax. TJ Hendrickson

Here is the filing that produced this victory for the rule of law. Brian Wright

Here is the filing that secured this victory for the law. Brian Wright

Here is the filing that produced this victory for the rule of law. Here, too, is a note to everyone else Brian asked me to post: Brian's Note To The Community. Ben in California

Here is the filing that secured Ben's victory for the law, and the California notice concerning his claim. Desiree Stumo

So, there's more to this refund than meets the eye. You see, Desiree made a monetarily tiny, but practically very significant mistake on her filing. When entering the amount of federal tax withheld on line 64 of her 1040, Desiree neglected to add the amounts withheld for Social security and Medicare surtaxes to the amount withheld under the generic expression "federal income tax". Desiree should have done so. ALL of these are federal income taxes, and if one didn't receive the "wages" on the alleged basis of which nominal federal income taxes get withheld, then one didn't receive the "wages" on the alleged basis of which the FICA taxes can properly be withheld. NOW, NORMALLY, a mistake like Desiree's is happily capitalized on by the IRS (literally). The agency just keeps what has not been reclaimed, despite surely being cognizant of the error, and that the FICA amounts are not owed. It is then rudely left to the claimant to go to the trouble of filing an amended return to get the rest of his or her money back. But not this time. This time someone at the agency took it upon him or herself to correct Desiree's calculations by adding the withheld Social security and Medicare taxes to her claim and cutting her refund check for the whole amount. Here is Desiree's filing. Look at the withheld amounts on the 4852s, the refund claim on page 2 of the 1040, and the amount refunded on the check proudly shown here and above by this fine young American grown-up. I say "Hats Off!" to this unknown bureaucrat. He or she has proven that real Americans can be found even where one might least expect (or that the people in the agency have been paying attention to what they, too, have had the opportunity to learn over the last 14 years).

James Lambert

This is the educated filing that produced this complete refund.

Mike & Angi Gangestad

Here is the filing that produced this victory-in-progress in which the feds acknowledge that Mike and Angi did nothing subject to either the normal tax or the FICA sur-taxes contrary to what is reported on their return, but lie about the amount withheld and seek to keep the FICA sur-tax withholdings anyway, obnoxiously forcing Mike and Angi to take further measures to recover their property. Patrick Hart

This notice was the culmination of a federal effort to snooker more than $10K from Patrick by way of this proposed effort in resistance to Patrick's educated filing concerning 2015.

Matt & Katie

Matt & Katie secured this complete refund with this return, after dealing with this little "identity-challenge" speed-bump.

Sandy D.

Here is the filing that secured Sandy's victory for the law. The Walkers  Here is the filing that produced this second complete refund in as many years for the Walkers. (As indicated at the bottom of this overpayment acknowledgement/refund and interest notice, this year's North Carolina refund for the Walkers was diverted to retire an alleged outstanding liability to Uncle Sam and thus didn't take the form of a check.)

Martha B.

Martha's victory was secured by way of this filing (in which Martha, for reasons of her own, chose not to claim back what had been withheld as the Medicare surtax). Note that the United States properly added interest to Martha's refund.

Click here to return to the Bulletin Board

Even in the face of the requirements of the law, the junkyard dog still tries to play its losing hand occasionally. Ironically, it is these sporadic spasms of resistance that offer the most telling evidence of the truth about the tax...

Despite the fact that those whose victories are on display here did nothing but insist that the law be applied as it is written, they did so in the face of fearful threats and cunning disinformation from the beneficiaries of corruption. Their actions took great courage and commitment, and I salute them all.

“God grants liberty only to those who love it, and are always ready to guard and defend it.”

-Daniel Webster

NOTE: Whether any given individual is entitled to a refund depends on a number of different factors, and no one should presume that they are so entitled simply because they see that others are. Each person should educate himself or herself about the particulars of the law, and make his or her own determination in this regard.

To get on the Lost Horizons mailing list, send an email to SubscribeMe 'at' losthorizons.com with your name in the message field.

NOTE: The documents displayed on this and any linked pages, and any associated comments, are posted with the permission and cooperation of the upstanding Americans with whom they are concerned. When a return is posted in connection with any refund or other responsive document, it is complete-- that is, what is posted is EVERYTHING filed as a return in connection with that refund or document, unless otherwise indicated. |

{kind=link}