|

More Victories For The Rule Of Law- Page Seventy-Four

Hundreds of thousands of readers of 'Cracking the Code- The Fascinating Truth About Taxation In America' have taken control of their own resources, in accordance with, and respect for, the law. The total amount reclaimed by these good Americans so far is upward of several billion dollars.

A few of these good American men and women-- such as those honored below-- are generous enough to send me the evidence of their victories in upholding the law, for the edification and inspiration of everyone. Walt & Maryanne WALT & MARYANNE SHARE A NICE VICTORY in recovering everything withheld from them and given over to the feds during 2022, Social security and Medicare taxes included, plus interest:

Here is the claim by which this victory in enforcing the law was secured. WELL DONE, WALT & MARYANNE!! LANCE HAS SECURED TWO recent victories: an outright complete refund from Arizona of everything withheld during 2022, and a victory-in-progress (v-i-p) from the feds for 2022, including only a partial refund thus far but acknowledging on paper that no "income" has been received and no tax is owed-- even the amounts yet to be refunded. Here is the Arizona refund:

...issued pursuant to this claim; and here is the federal refund notice and acknowledgement:

...issued pursuant to this claim. As is typical in these v-i-p cases, the refund notice blatantly lies in a couple of key respects apparently meant to confuse the target. Specifically, on the first page of the notice under the heading, "Why we changed your information", it says, "We changed the amount claimed as federal income tax withheld on your tax return to reflect the amounts shown on Form(s) W-2, 1099, or other supporting documents." But the supporting documents (that is, the Forms 4852 attached to the 1040 in support of the refund claim) show $17,471 withheld as federal income tax in total. This falsehood is emphasized with the follow-up lie on page 2 of the notice. There, under the heading, "Your payments and credits", it says "Income tax withheld, Form 1040 line 25d" and lists $11,412, whereas the figure actually appearing on Lance's 1040, line 25d is the full $17,411 withheld. The hope appears to be that Lance will be misled into imagining that for some reason even though everyone agrees that he did nothing taxable the feds still get to keep the FICA income surtaxes withheld from him, and that they aren't even proper to list as having been withheld at all-- even thought the law expressly commands otherwise: Any tax paid under chapter 21 or 22 by a taxpayer with respect to any period with respect to which he is not liable to tax under such chapter shall be credited against the tax, if any, imposed by such other chapter upon the taxpayer, and the balance, if any, shall be refunded. ...and the IRS admission that Lance had no "wages" under Chapter 24 of the IRC (an admission expressed not only in the agency's black-and-white statements in the notice above, but also by its having returned to Lance everything withheld from him pursuant to that chapter) is also an admission that Lance had no Chapter 21 "wages" by which any FICA tax liability can be measured and established-- a point recognized by the US Supreme Court in Rowan Cos. v. United States, 452 US 247 (1981), in which it is held that "wages" under Chapter 24 are the same thing taxed as "wages" under Chapter 21 and 22, meaning that if one hasn't had the former, one cannot have had the latter. (See that all explained in detail here.) Lance still has a bit of a battle in front of him to get the rest of his money returned (or at least the submission of a firm demand in light of the foregoing), but meantime, WELL DONE, LANCE! Paul & Rebecca Greene PAUL & REBECCA SHARE THEIR VICTORY with the state of Virginia in securing the return of everything withheld from them and given to the state during 2022, plus interest:

Here is the return by which this victory was secured. WELL DONE, PAUL & REBECCA!! Lynda Thorne LYNDA HAS SHARED her debut victory as an educated American tax return filer, recovering everything withheld from her and given over to the feds in 2022, plus interest:

Here is the filing that secured this victory for the rule of law. WELL DONE, LYNDA!! Justin & Brianna Gilmore JUSTIN & BRIANNA SHARE THEIR LATEST VICTORY, this time over Colorado, for 2022, and not of "income tax" withholding, but of sales tax withheld, which Colorado law refunds when overall "income" receipts are below certain threshholds:

Here is the filing which secured this refund. WELL DONE, JUSTIN & BRIANNA!! Craig & Wanda Lorenz CRAIG & WANDA SHARE THEIR LATEST VICTORY-- this one over Michigan for 2022:

Here is the filing by which this victory was accomplished, and... WELL DONE, CRAIG & WANDA!! Jeff Rische JEFF RISCHE'S VICTORIES are always especially significant and worthy of note. You see, for a number of years now this excellent American has not only won victories but has also prosecuted a series of litigations against various abusive IRS practices during which the "ignorance tax" schemers have been forced into numerous evasions and contrivances in their desperate effort to shore up the fraud. A few years ago, one such litigation commenced over the assertion by the IRS of a "frivolous return penalty", based on the "ARG44" hoax (discussed in detail here), in regard to Jeff's claim for amounts withheld during 2018 (which had never been honored). Although a number of victories on the hoax issue have recently been accumulating, in this case Jeff went all the way up to the 9th circuit (where he is well known due to those other litigations) with no joy. Instead he found repeated shameful judicial dodges, with the matter being closed out by the court last May. Nothing out of the ordinary in the foregoing, for the most part, but on July 10, 2023, Jeff found in his mailbox two notices from the IRS. One is a v-i-p refund of Jeff's claim for 2018, plus interest:

The other is a v-i-p refund of Jeff's claim for 2020 (strangely, sans interest):

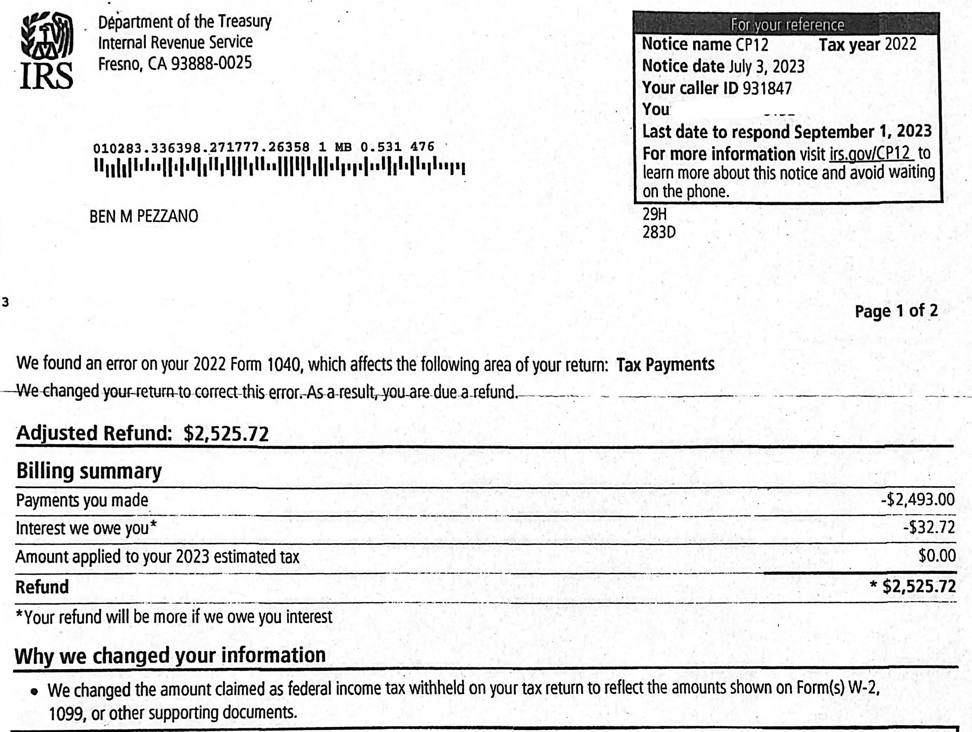

Here is the 2018 filing; and here is the 2020 return. You've got to love the implications. Understand that just because these particular refund notices don't spell out the "$0 income, $0 tax owed" found on the CP16 sent to Lance Cole posted above, they carry the exact same meaning. The refund in full of amounts withheld pursuant to Chapter 24 against purported "wages" is an admission that no such "wages" were received by Jeff, and that, in turn, means that no Chapter 21 "wages" were received, either-- which in turn means that no tax under any label arose or is due (and yet the surtax withholdings are being kept by the government anyway, so far). At the same time, the IRS is pretending that Jeff's returns meet the statutory specifications of "frivolous" for the application of the "frivolous return penalty", while having admitted that his filings are correct in every respect. Further, by having resorted to the fake "frivolous return position" allegations, the IRS has also admitted that no actual statutorily-specified qualifying position by which the penalty can validly apply can be asserted about Jeff's filings. The agency is tying itself in knots, or, rather, Jeff is tying the agency in knots, and the corrupt courts, too. WELL DONE, JEFF-- VERY WELL DONE!! BEN FILED NOT ONLY an educated return and claim concerning 2022 withholding totaling $7,884.03 early this year (albeit with a little confusion over the proper way to rebut an erroneous K-1). He also provided a very clear cover letter explaining his filing. (See both here.) Nonetheless, the first response by the IRS was to try its ridiculous and corrupt pretense of acknowledging that Ben had had no tax-relevant "income" and owed no tax, but was somehow entitled to keep what had been withheld from him as Social Security and Medicare taxes (by pretending that those amounts had not been withheld, or don't qualify as "federal income taxes", and falsely reporting the amount shown on line 25(d) of Ben's 1040 to be only $2,493 (just as discussed more fully here in regard to the same corrupt treatment visited upon Lance Cole):

Immediately upon receiving the partial refund pretense, Ben, drawing on the comprehensive legal resources I have presented in my books and on LHC over the last 20 years, fired off this cogent and concise reply, spelling out the relevant law and facts in detail, and demanding proper treatment by the tax agency. The IRS responded with a bizarre, disconnected letter about an amended return, seen here. Again, Ben fired off a straightforward and sensible reply pointing out the relevant facts and making clear that he was a grown-up American fully committed to standing his ground and enforcing the law. After these exchanges helped the IRS see the light, the agency finally threw in the towel and got right with the law, returning all of Ben's money, with interest:

WELL DONE, Ben! Brett & Tori Lackey BRETT & TORI'S partial refund for 2022 from the feds was posted in the July 17 Newsletter, with a claimed $27,188.64 yielding just a $7,435.36 refund to begin with, on the same absurd pretense as that used against Ben Pezzano. But like Ben, Brett & Tori weren't having any of it. After getting that first deposit, Brett & Tori fired off a letter spelling out the relevant facts and law. The IRS responded, but breaking the pattern a bit, this response was not just previously typical stonewalling, stalling, or gibberish. Instead, the agency tried to snake out of this problem with yet another partial refund of $10,776.59 more of what is owed to our virtuous warrior couple, followed by a notice purporting to explain the new deposit:

Brett & Tori, making progress but still short of made whole, again wrote an admirably patient reply, again explaining the facts and the law. This time the IRS response since then has been a stall letter, followed a month later by a complete bit of nonsense pretending that Brett & Tori had tried to claim a refund of "Excess Social security Railroad Retirement tax" withheld (a subject discussed here, and in no way relevant to Brett & Tori's filing. So, Brett & Tori aren't quite done with this silly little tussle, but the IRS is losing ground-- and dignity-- rapidly. WELL DONE, Brett & Tori! Julie Ann Marien JULIE ANN SHARES TWO nice victories today. Let's start with her recovery of everything withheld from her and given over to the feds during 2020, secured, with interest, by way of an amended return:

Julie Ann follows up with a victory-in-progress from the feds for 2022, in the form of an admission of no tax-relevant "income" received, and no taxes owed, despite which the IRS is still trying to suggest that Julie Ann is not entitled to a complete refund:

This corrupt ploy is in response to this filing, which was first met with a little bit of pothole-style resistance (showing, among other things, that the tax agency had looked closely at Julie Ann's return before issuing that admission and partial refund, above), to which Julie Ann had patiently replied with this. In October, Julie Ann wrote again, specifically addressing the CP12 admissions and fabrications/omissions/mendacities, to which she is still awaiting a response. But those admissions have been made, and as seen above, the v-i-p ploy is crumbling. We will expect further good news, but in the meantime, WELL DONE, Julie Ann! Deborah Smith DEBORAH IS ANOTHER educated filer unwisely targeted by the IRS for the v-i-p treatment. Here is Deborah's filing for 2022, plainly showing and supporting a complete refund claim of $11,704.00. The desperate, mendacious (but critical and self-defeating admission-laden) IRS response? Behold:

As I said, I don't think Deborah was a wise choice of American to target with this bs. We'll see what happens, but I think it'll be more than $17.50 for Deborah in the end. Meantime, WELL DONE, Deborah! John & Mercy Polhemus JOHN & MERCY POLHEMUS have shared the debut educated-filing refund secured for 2023 (or, at least, the first one shared with me for sharing with you, anyway). John & Mercy got busy filing their educated return in February, and two weeks later received back everything withheld from them under the income tax laws and given over to the state of Maine last year:

Here is the filing by which the claim was made and the refund secured; WELL DONE John & Mercy!! JACQUES & PEGGY have secured the complete return of what had been withheld from them during 2021, along with what they had paid in that year in estimated tax payments and with their request for an extension in 2022, plus interest. All of this was by way of an amended return which was briefly resisted and then, after some no-nonsense prompting, honored in full. In fact, Jacques & Peggy's claim was more than honored, since after Jacques & Peggy's remonstrance of the agency's balkiness, the IRS corrected-- in Jacques & Peggy's favor-- a $10,000 error the couple had made in totaling up all those amounts when making their claim. First, let's enjoy Jacques & Peggy's nice refund:

Here is the filing by which this return of property was secured, which includes this very cogent explanation as requested on the 1040X involved:

NOW, AS NOTED ABOVE, this victory has a few quirks to discuss-- all of which are good! To begin with, the first IRS response to Jacques & Peggy's filing (on March 1, 2024) was to say, "Thanks for your amended return; we've adjusted your account as requested; the adjustment changes nothing." Here is how this strange self-serving gibberish was put:

Jacques & Peggy wasted no time responding calmly and confidently, if with a bit of perfectly reasonable tartness:

The IRS response to this March 9, 2024 letter was to issue, a week later, the interest-bolstered check you see above. But that's not all. The chastened tax agency, apparently recognizing that it was dealing with serious, well-educated and resolute American grown-ups, took an extra step (even if only one which was ethically proper in any case). You see, Jacques & Peggy, though doing everything right overall, and clearly in command of the situation, made a simple math error in their filing. As seen in the computation of amounts paid/withheld and refund claimed on their return, shown here:

...the "total payments" figure on line 17 failed to include $10,000, being added up and reported as $49,955 instead of the correct figure of $59,955-- a forgivable mistake anyone could make while completing a form many find fairly confusing in its layout, and which was probably the first 1040X Jacques & Peggy have ever filled out. This mistake also manifests in the recital of the facts these good folks made in their reply to the IRS's initial dodgy letter. Not to worry, though. The now law-abiding tax agency stepped up right and proper, and corrected Jacques & Peggy's mistake, adding in the missing $10,000 to the amount claimed by the couple and including it in the refund check-- a happy fact which sharply emphasizes the close attention paid to the details of Jacques & Peggy's claim before that claim was plainly acknowledged as soundly-based in the law and the facts and honored in full. WELL DONE, Jacques & Peggy (and WELL DONE, IRS)!! Click here to return to the Bulletin Board

Even in the face of the requirements of the law, the junkyard dog still tries to play its losing hand occasionally. Ironically, it is these sporadic spasms of resistance that offer the most telling evidence of the truth about the tax...

Despite the fact that those whose victories are on display here did nothing but insist that the law be applied as it is written, they did so in the face of fearful threats and cunning disinformation from the beneficiaries of corruption. Their actions took great courage and commitment, and I salute them all.

“God grants liberty only to those who love it, and are always ready to guard and defend it.”

-Daniel Webster

NOTE: Whether any given individual is entitled to a refund depends on a number of different factors, and no one should presume that they are so entitled simply because they see that others are. Each person should educate himself or herself about the particulars of the law, and make his or her own determination in this regard.

NOTE: The documents displayed on this and any linked pages, and any associated comments, are posted with the permission and cooperation of the upstanding Americans with whom they are concerned. When a return is posted in connection with any refund or other responsive document, it is complete-- that is, what is posted is EVERYTHING filed as a return in connection with that refund or document, unless otherwise indicated. |